Overview

The resolution of the debt-ceiling debate, in early June, together with somewhat encouraging economic news throughout the month contributed to propelling equities forward worldwide.

In June, the S&P’s 500 rose a potent 6.61%. The Nasdaq Composite added 6.65% to an already impressive performance in 2023. Finally, the Russell 2000 (Small Cap Stocks.) added 8.31%. With the European Central Bank pushing their intervention rate up .25% and the Fed on pause this month, the USD dropped a little over 1% against a basket of major currencies. This helped support otherwise less exuberant international equity markets. The EPAC BM Index of developed economies (ex-US) rose 4.09% in June, while emerging markets added 3.23% (MSCI EM).

US bonds were generally stable with the US bond aggregate index down a mild .36% and corporate bonds adding from .41% to 1.67% for the Bloomberg Corporate Index and its High Yield counterpart respectively.

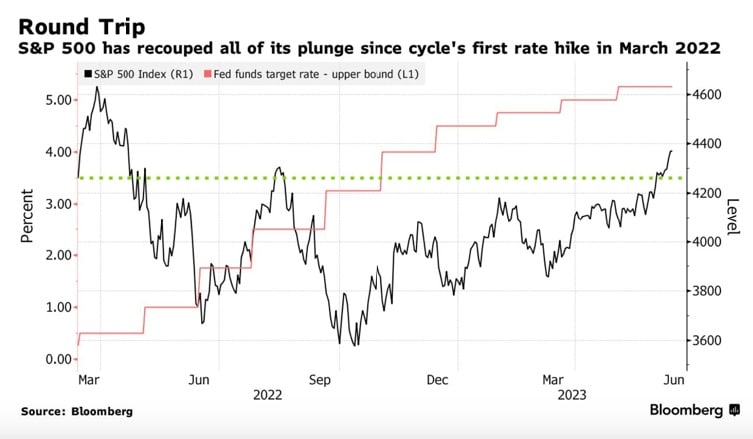

The chart below illustrates the market recovery since the end of September 2022. While the S&P’s 500 has not yet reached its 2022 peak, its recovery has nonetheless been spectacular and somewhat unexpected, given the drumbeat of sobering economic and geopolitical news over the past eighteen months.

In June, our median portfolio grew 3.64%. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 2.71%. YTD, our median account is up 7.67% vs. 8.23% for our reference index.

Market developments

A mixture of moderately encouraging economic news, alternatively related to inflation and growth, punctuated the month of June and ended up contributing to the spectacular performance mentioned earlier. The FED’s decision, widely expected, to keep its intervention rate unchanged (between 5% and 5.25%) also helped.

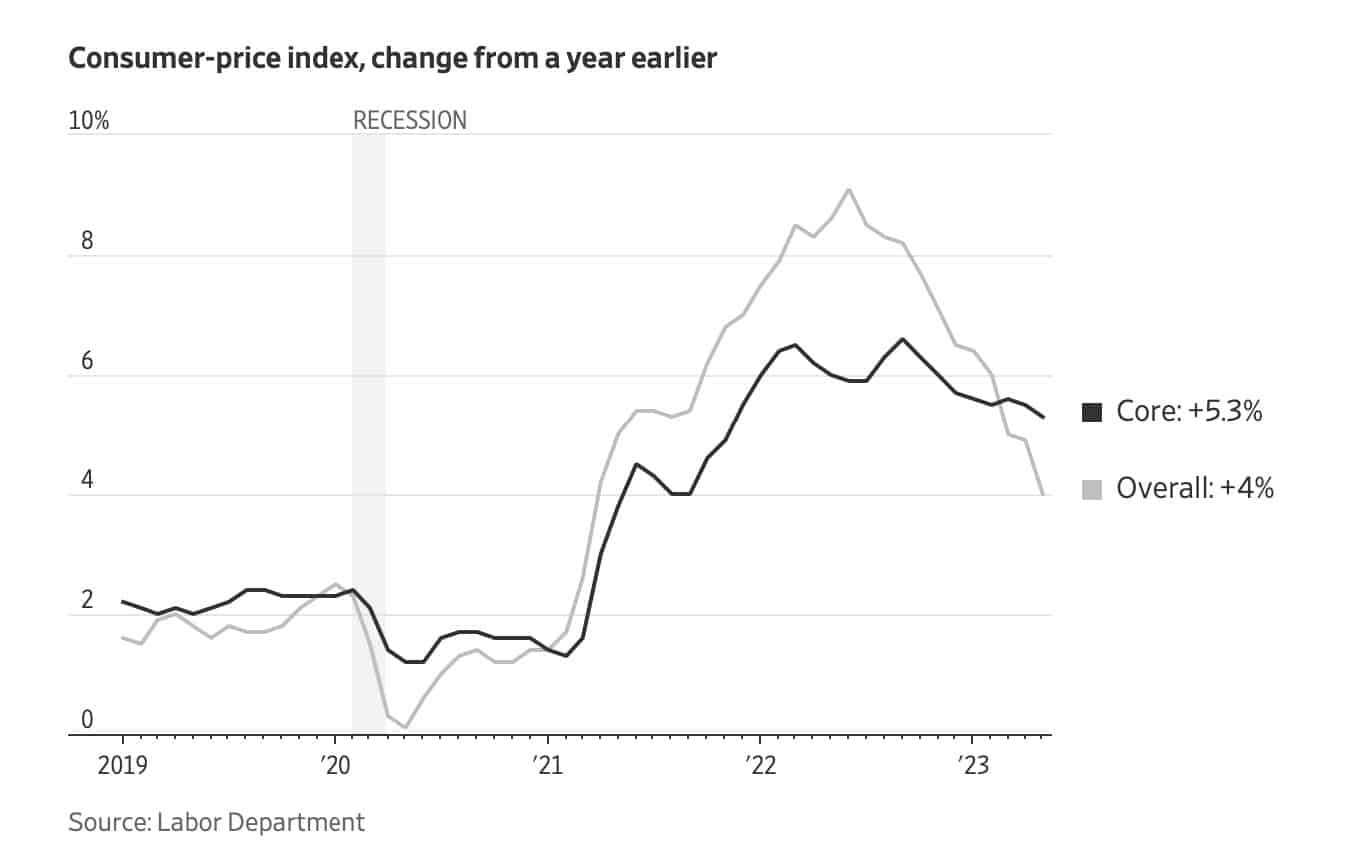

The chart below illustrates where we stood with respect to the fight against inflation, as of mid-June:

Overall inflation stood at a little over 4% at the end of May. However, core inflation (a measure of inflation that strips it of its highly volatile components, particularly energy and food prices) remained somewhat elevated. Further, its decline has been stubbornly slow. Since this is the measure of inflation that informs the FED’s decision, the likelihood of further fed funds hikes is high. As a matter of fact, the FED has indicated that two further (.25%) hikes are likely between now and the end of the year. The probability that the first of them will take place at the end of July is currently at 80%, based on a recent poll of market economists.

I have mentioned in previous newsletters that the chance of the FED “overdoing it” is real. Its resolve to bring inflation down to a 2% long-term trend may cause it to break the back of the US economy in the process. The fact that this has not happened yet explains in good part the performance of US equities this year.

Tilts and Allocations

In June, I effected a small rebalancing within our US equities allocation. I sold a little bit of our QQQ investments in favor of VTV, so as to keep both exposures equal.

If you recall, QQQ, is the NASDAQ 100 ETF. It is laden with tech stocks (read “growth”) and has risen more than 20% since mid-March when we bought it. VTV is the “value” ETF that we invested your portfolio in, in equal proportion to QQQ and at the same time. Since then, QQQ has progressed 25 % and VTV only 5%, giving it a somewhat outsized place in each portfolio.

The chart below illustrates the progression of each ETF since the time of purchase:

Our intent in effecting this re-balancing was to keep each factor (growth and value) at an equal weight.

Elsewhere in our portfolios, SCHW added 7.5% in June while Air Liquide added 6.30% and the modicum of exposure that we have to Bitcoin rose a spectacular 38%.

Most portfolios have less that 1% invested in Bitcoin (in GBTC, the Bitcoin investment trust, to be specific). That diminutive allocation is meant to protect them from a repeat of what we saw in 2022 when Bitcoin lost close to 80% of its value. At the same time, it is also meant to benefit on occasion from the incredible (positive) volatility of the crypto space. In June, we benefitted from such a move.

Conclusion

At the beginning of the year, and after awful portfolio performances in 2022, the constant talk of impending economic recession was so loud that it took investors some nerves to remain meaningfully invested in equities.

So far this year, that steadfastness has paid off. Not listening too much to economists and market pundits (particularly those on TV), is a must when investing in markets.

Now, twice a day, even a broken clock tells the truth. At some point, we will have a recession.

If you are one who believes that raising interest rates automatically fosters one, a recession within the next few months is quasi-certain. If you are like me and think that this Covid-induced bout of inflation is something very different from what we have ever experienced, you are not so sure that it will come about so rapidly. So far, it has not materialized.

In my view, the risk now is that the FED sticks to its austere monetary policy for too long and does not give itself enough time to see its (successful) effects on inflation.

Please feel free to reach out to me with any questions.

Thank you for your continued trust and Happy Fourth of July!

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980