Overview

In May, the S&P 500 gained a whopping 6.29% overall while the Nasdaq composite rose 9.65% and the Russell 2000 (Small Cap stocks) gained a comparatively meager 5.34%. Another series of tariff reversals from the Trump administration and robust first-quarter earnings results from major companies in the tech sector explain this spectacular performance.

Internationally, the EPAC BM Index of developed economies (ex-US) gained 4.36% while emerging markets progressed to a lesser extent, the MSCI EM (emerging markets) rising 4.00% and the MSCI Frontier 100 index 4.19%.

To put things in perspective, below is a chart that summarizes the performance, Year-To-Date (YTD), of the S&P 500 and of the Nasdaq:

In the end, YTD, US equities have not progressed and the sharp stock upward momentum started in mid-April has only allowed for a recovery of the ground lost since the announcement of “Liberation Day” in early April.

In May, US fixed income markets declined a bit, particularly at the long end (long-term bonds) as fears of a runaway budget deficit rose with the House’s approval of the “Big, Beautiful tax bill” that, by all independent measures, add trillions to the US deficit.

The AGG index finished the month with a small loss of .72%, while Investment Grade and High Yield bonds managed gains of, respectively, .01% and 1.68%. The Bloomberg municipal index was flat.

Our median portfolio was up 1.43% in May. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) gained 2.54%. Year to Date (YTD) our median portfolio is up 1.84% vs. 3.89% for our benchmark.

Market developments

The relative attenuation of the tariff rhetoric coupled with solid tech earnings for the first quarter of the year, released throughout the month of May, explain in large part the sharp stock rebound in May.

In addition, hard economic data, such as the unemployment number, released early in the month, or inflation, released at the end of May, both failed to show a deterioration of the economy. The April unemployment numbers came in a bit better than expected. As for the Personal Consumption Expenditure (PCE), the inflation metric favored by the Federal Reserve (FED), it continued to remain in line with expectations, running at a 2.5% annual rate.

Yet, tariffs will have an impact on inflation and investment decisions and DOGE will impact employment. At some point, these policies and decisions will translate into hard economic effects.

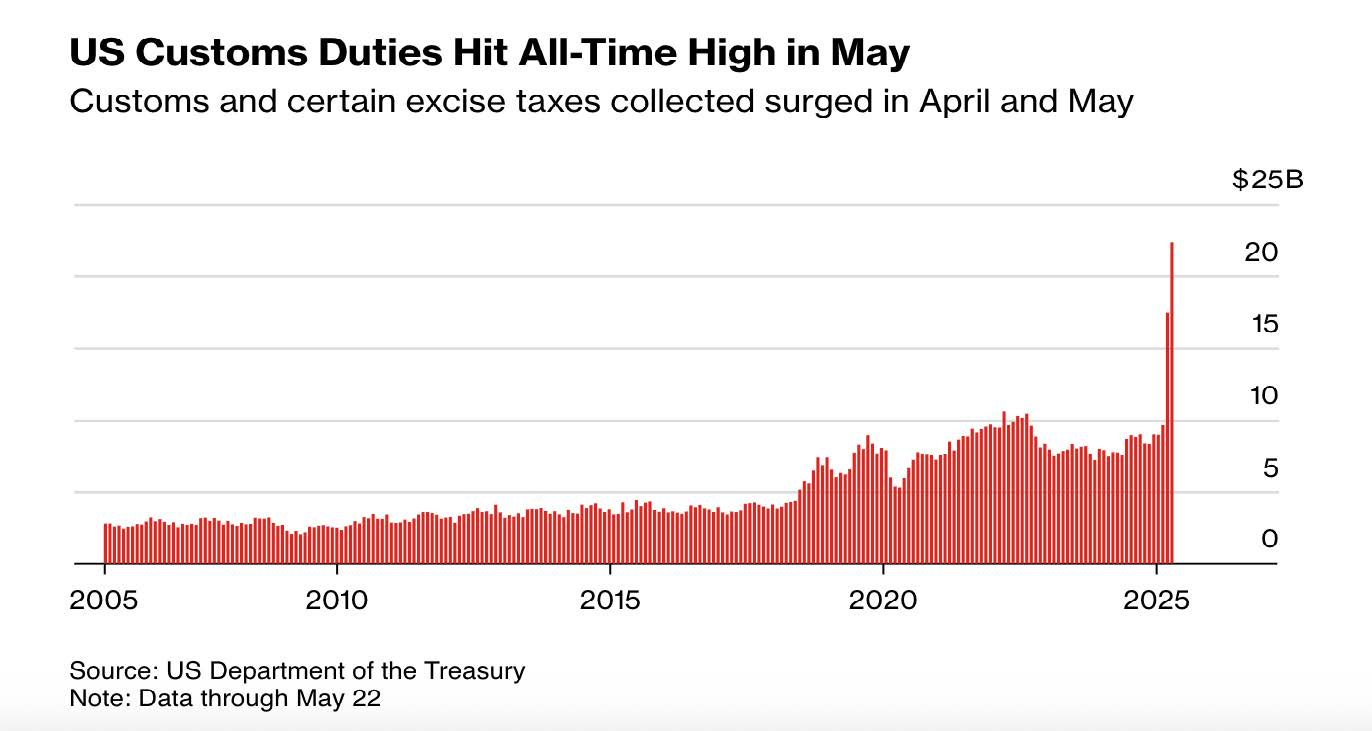

For now, the chart below shows that the Trump Administration’s tariffs policy is having an impact on public finances:

It is unlikely that the economic players paying those duties (importers) will absorb all the costs paid to the government.

Eventually, the US consumer will start feeling them. How will overall consumption be affected remains the big question. Equity markets seem to have ignored it or set it aside for now. Choosing instead to focus on good corporate earnings.

Portfolio Commentary

In May, I maintained our equity allocation well below our usual levels. As a result, we did not fully participate in the sharp bounce in tech and other sectors. I am not convinced that this market recovery has “legs” and will endure.

This is why, in May, I mostly reinvested maturing US Treasuries. Some portfolios saw their allocation to gold (IAU) increase). But other than these “risk-adverse” measures, I refrained from jumping back in.

While hard data on consumption has shown some softening, as indicated in the chart below, more is needed for investors to pay attention and to reduce their allocation to equities.

For now, tech results are all that matters. How long will this behavior continue to ignore other factors such as tariff induced inflation (a possibility) or delayed investment decisions (a corporate reality) remains to be seen.

Perhaps the bond market is going to prompt the kind of awakening that I anticipate and fear. The US budget deficit will increase substantially should Congress pass Trump’s “Big, Beautiful” bill. The bill will add trillions to the deficit. The bond market is starting to worry, as shown in the chart below:

The steepening of the yield curve that this chart underlines indicates that bond investors will require higher returns to invest in US debt, making it costlier for all of us to borrow, consume and plan.

Conclusion

I find myself in the uncomfortable position of managing clients’ assets at a time when markets are rising while the economic and political environments remain highly uncertain.

This lack of visibility explains my prudent investment posture. I would expect this situation to change once the effects of “Liberation Day” and of the “Big, Beautiful Bill” have been properly weighed. The course should be clearer then and with it an increase in our equity allocation more justifiable.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980