Overview

Political and economic uncertainties continued to plague market sentiment in April. In the end though, equities were little changed. The S&P 500 lost .68% overall while the Nasdaq composite inched up .88% and the Russell 2000 (Small Cap Stocks) lost 2.31%.

Internationally, a weakening USD helped developed markets fare much better than their US counterparts. The EPAC BM Index of developed economies (ex-US) gained 4.43% while emerging markets progressed to a lesser extent, the MSCI EM (emerging markets) rising 1.34% and the MSCI Frontier 100 index .88%.

This month saw investors making major adjustments to their portfolios, as illustrated in the chart below:

As the Trump Administration announced its intention to inflict punitive tariffs on geopolitical foes and friends alike and then partially reversed itself, investors made a few important decisions: 1) move out of USD assets, which caused the USD to decline 4.30% against a basket of major currencies, 2) go into gold and other “safer” investments. I think that given the severity of the damage caused by the US administration to international relations, these investment decisions are not likely to be reversed soon.

In April, US fixed income markets held up generally well. The AGG index finished the month with a tiny .39% gain, while Investment Grade and High Yield bonds suffered modest losses, respectively .03% and .02%. The Bloomberg municipal index was down .81%.

Our median portfolio was down .41% in April. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) gained .48%. Year to Date (YTD) our median portfolio is up .23% vs. 1.38% for our benchmark.

Market developments

The Trump Administration’s unique approach to international economic and political relations caused markets to tumble at the beginning of April. Fears of a global economic slowdown sent US equities down 15% in two days. A partial reversal, in the form of a 90-day tariff reprieve and the promise of one-on-one negotiations with trading partners, reassured investors. By the end of the month, US equities had clawed back the bulk of their earlier losses.

Economic players, be they corporations or investors, do not like uncertainty. Uncertainty leads to investment decisions being postponed or cancelled, among other things. Postponed or cancelled investments lead to economic slowdowns.

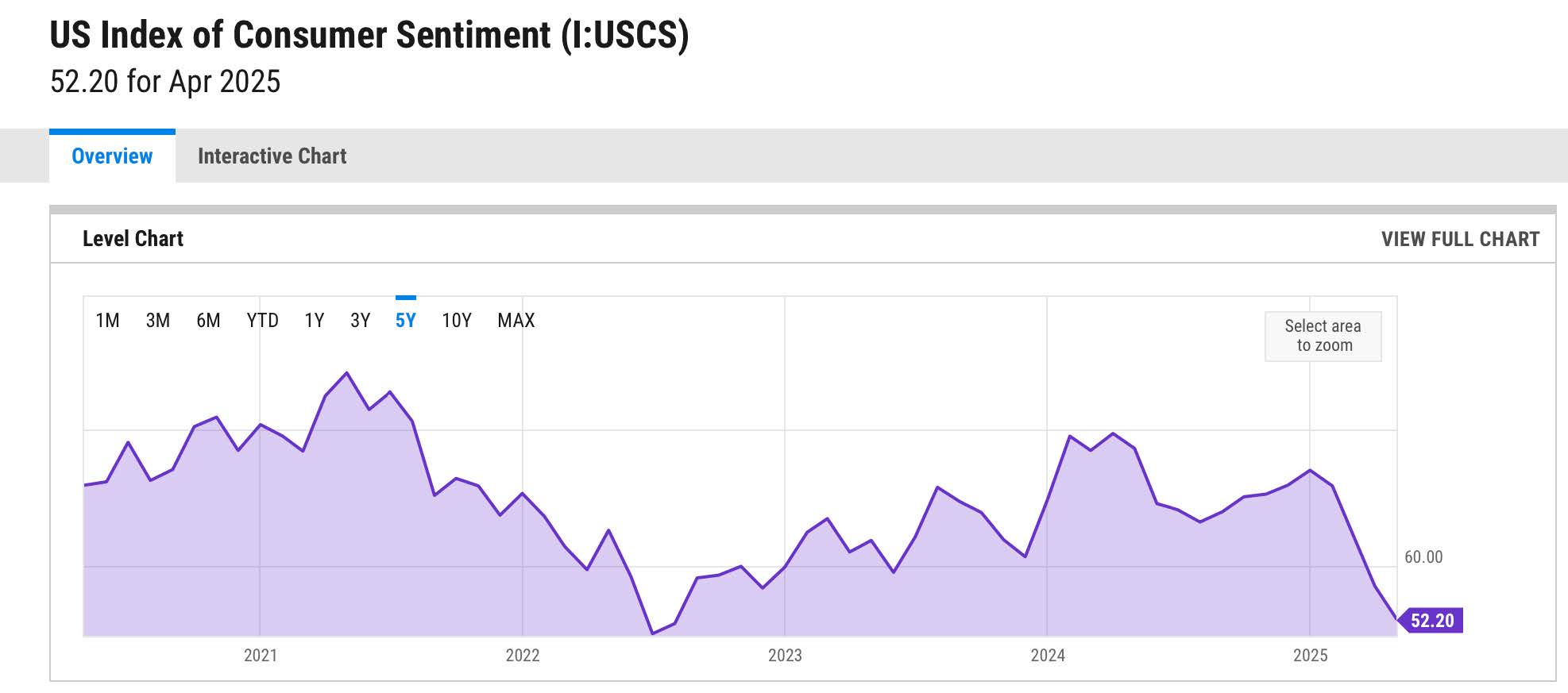

For now, the negative economic effects of heightened uncertainty are not yet visible other than in “soft“ economic data, such as the index of Consumer Confidence, shown below:

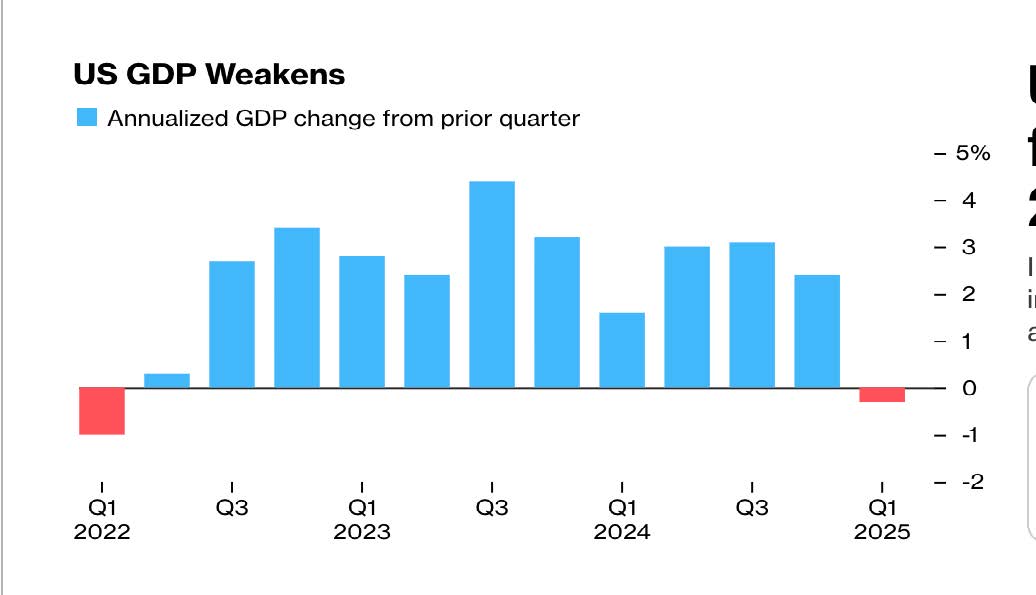

Consumer confidence is at its lowest since the middle of the Covid pandemic. Other metrics, such as unemployment or GDP, shown below, remain mixed. While both are weakening, they are doing so at a measured pace:

The negative GDP first quarter number can be largely explained by anticipatory purchases of imported goods, ahead of higher tariffs. For now, investors feel unmoved.

Portfolio Commentary

In April, I cut our US equity allocations by 5% to 10% across all portfolios. I used the proceeds to add to our gold holdings and to our fixed income investments. Specifically, I increased our investments in short-term US treasuries and in AGG, the US bond aggregate ETF.

These decisions, intended to reduce our overall risk level, caused us to underperform slightly vs. our benchmark this month as the US tech sector bounced in the last ten days of the month and the Trump Administration toned down its confrontational trade rhetoric.

I believe that this is a welcome respite but doubt that it will last much longer.

The damage done by the constant threats and attempts at extorting other nations is starting to be felt politically around the globe. Against the odds, Canada re-elected a liberal PM and Australia is in the process of doing so, as I write this letter.

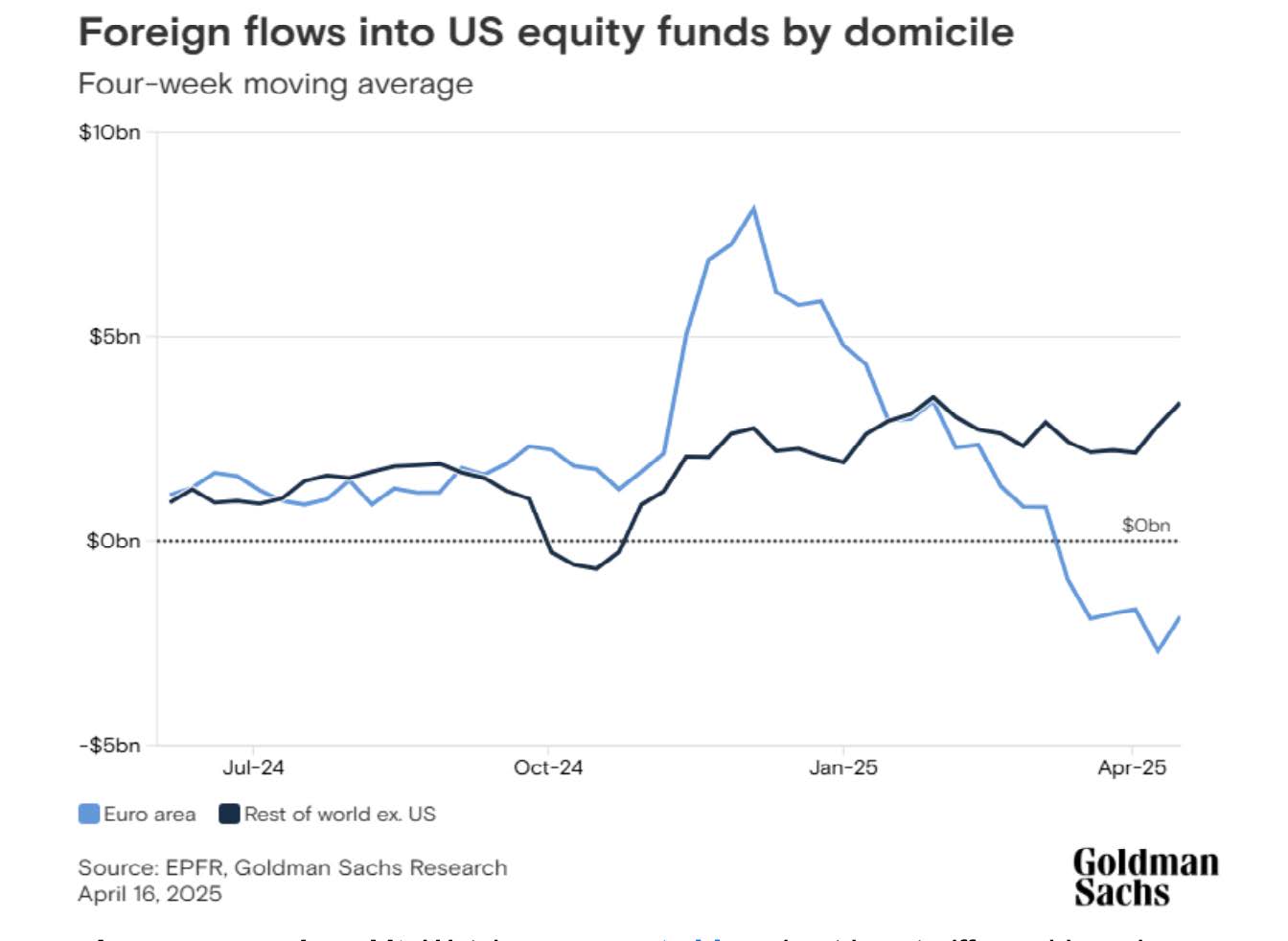

From an investment point of view, the damage is starting to be seen and measured, as shown below:

The Trump administration appears to respond to deteriorating economic conditions and wobbly markets more than to anything else. Perhaps a further weakening of the USD and/or the fear of sustained dislocation of the US Treasury market, will prompt lasting stylistic as well as substantive changes. In the meantime, US investors are likely to suffer or, at a minimum, to remain on edge.

Conclusion

We are entering a period of the year that is traditionally associated with tepid equity market performance. “Sell in May and go away”, so goes the adage.

I am not going away. I will maintain a very prudent posture over the foreseeable future and do not anticipate any major changes to our portfolios. Economic and political uncertainties are so elevated that I do not plan to increase equity allocations any time soon.

About the only things that could lead me to reconsider would be a sustained rally, a major reversal in economic policy or clear congressional support for the Rule of Law in our country. A support that, so far, has been shockingly muted.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980