Overview

In June, the S&Ps’ 500 positive momentum continued, pushing up monthly performance another 5.09% overall while the Nasdaq composite rose 6.64% and the Russell 2000 (Small Cap stocks) gained 5.44%. A quieting down period orchestrated by the Trump Administration on tariffs, together with supportive or equivocal economic metrics, explain in part the spectacular move upwards, in spite of a complex geopolitical and national environment.

Internationally, the EPAC BM Index of developed economies (ex-US) gained 3.07% while emerging markets progressed in line with US indices. The MSCI EM (emerging markets) rose 5.65% and the MSCI Frontier 100 index added 4.03%.

To put things in perspective, below is a chart that summarizes the total return performance (dividends reinvested), Year-To-Date (YTD), of the S&Ps’ 500, of the MSCI ACWI (all country world index) and of the US bond aggregate:

US equities have bounced back sharply since early April (Trump’s “Liberation Day”) as indicated by the orange line. However, they lag behind the ACWI (purple line) due to the significant slide of the USD since the beginning of the year. The Blue line shows the YTD performance of the US bond aggregate, a proxy for the US fixed income market.

In June, US fixed income markets rose on the expectation of incoming FED interest rate cuts. The fixed income markets have gone up and down since the beginning of the year, as those expectations wax and wane. As of this writing, the FED is not expected to cut interest rates before the end of September, at best.

Our median portfolio was up 1.97% in June. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) gained 3.13%. Year to Date (YTD) our median portfolio is up 4.06% vs. 7.17% for our benchmark. Our “risk-off” posture since mid-February is causing us to underperform when equities rise sharply as they have over the past two months.

Market developments

Navigating markets is rarely a simple exercise. Lately, it has become particularly challenging.

The totality of the economic picture remains blurry. At times, markets sense that the economy is slowing down, yet unemployment numbers do not move up much and consumption remains relatively stable. At times, inflation creeps up but not decisively and not enough to ensure that the FED will not cut interest rates at some later point in the year. Adding to the uncertainty is the incoherence and/or gamesmanship of the Trump Administration regarding tariff and foreign policy or its attempt to influence independent agencies (the FED being one of them), for example.

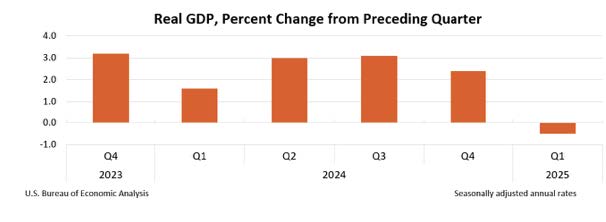

The charts below illustrate the mixed economic signals that investors have to contend with.

Inflation seems to be creeping up. But is it enough for the FED to maintain its restrictive policy (keeping interest rates as they are now)?.

And is the economy really slowing down as indicated in the chart below?

If it is slowing down, then the FED needs to reduce its Fed Funds rate to encourage consumption. If it is not, it should stay put.

The FED is in a tough spot. A wise and strong Fed Chair should continue to do what Chairman Powell is doing: nothing. Whether that lasts is anybody’s guess. With the Trump Administration talking openly about removing him asap since he won’t do their bidding, the FED’s independence is threatened and uncertainty increased.

Portfolio Commentary

I kept a risk-off posture in June. This explains our underperformance versus our benchmark index. It is likely to continue until I feel that we have gained some clarity with respect to tariff policy and to the status of the US economy. And specifically, whether it is in the process of contracting or not.

On July 9, the Trump Administration is supposed to impose steep tariffs on the nations and economic blocks that will not have abided by their bullying tactics. I am not sure what to expect. There is certainly no reason to invest ahead of that date unless one feels like gambling.

Additionally, third quarter corporate earnings will start to be released at the mid-point in July. Those earnings, as they are released over the following six weeks, will show whether corporate investment decisions have been impacted by tariff and policy uncertainty. We may also have more information concerning the inflationary effect of this uncertainty, if any.

At this juncture, and unless significant economic and/or geopolitical news cause me to change my view of the economic and of the overall situation, I do not plan to increase our currently low equity allocation to higher levels before September. By then, I would hope to have more clarity on where the Trump Administration is driving the US economy and the world’s economic and strategic alliances.

In the meantime, I will ask you to be patient with me and to endure the underperformance that this posture may cause when equity markets rally.

Conclusion

Have a good summer!

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980