Overview

In August, the S&Ps’ 500 positive momentum continued, pushing up monthly performance another 2.03% overall, while the Nasdaq composite progressed “only” 1.65% and the Russell 2000 (Small Cap stocks) gained 7.14%. The anticipation of a FED interest rate cut in September boosted the performance of the Small cap sector due to their financial leverage and the disproportionate benefit that this sector would derive from a rate cut.

Internationally, the EPAC BM Index of developed economies (ex-US) jumped 4.09% propelled by a declining USD. Emerging markets progressed in line with US indices. The MSCI EM (emerging markets) rose 1.47% and the MSCI Frontier 100 index added 4.41%.

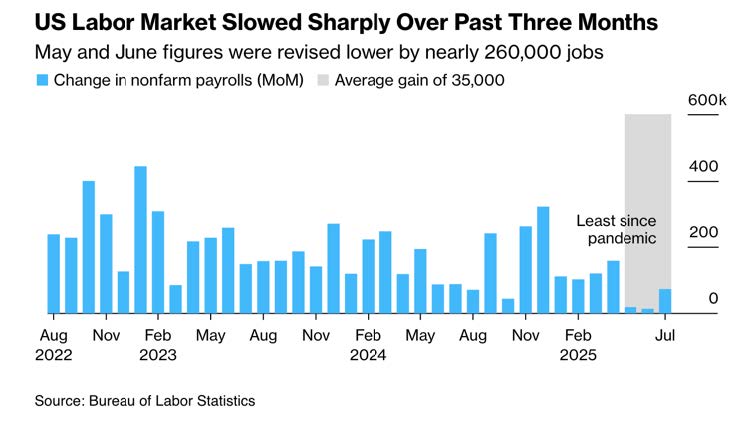

These developments arose in the context of increasing signs of a slowdown of the US economy, as illustrated in the chart below:

A sharp downward revision of the number of jobs created by the US economy in June and July caused the employment picture to become particularly worrisome. Of the dual mandate of the FED (to keep inflation in check around 2% and employment at the highest level possible given the inflation constraint), the FED seems to have decided now to favor maintaining full employment at the risk of enduring a higher level of inflation. Hence the favorable equity market response this past month.

US fixed income markets progressed in August. The US bond aggregate was up 1.20%. Investment grade and high yield corporate bonds gained 1.01% and 1.25% respectively.

Our median portfolio was up 1.92% in August. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 1.94%. Year to Date (YTD) our median portfolio is up 5.78% vs. 9.58% for our benchmark.

Market developments

The signs of a slowing US economy are increasing in numbers but, until very recently, investors appear to have largely discounted them in favor of robust corporate earnings and of an impending FED interest rate cut.

The last trading days of August though have reflected investors’ preoccupations with a counter narrative centered on an overvaluation of the tech sector and the effects of a slowing economy on markets.

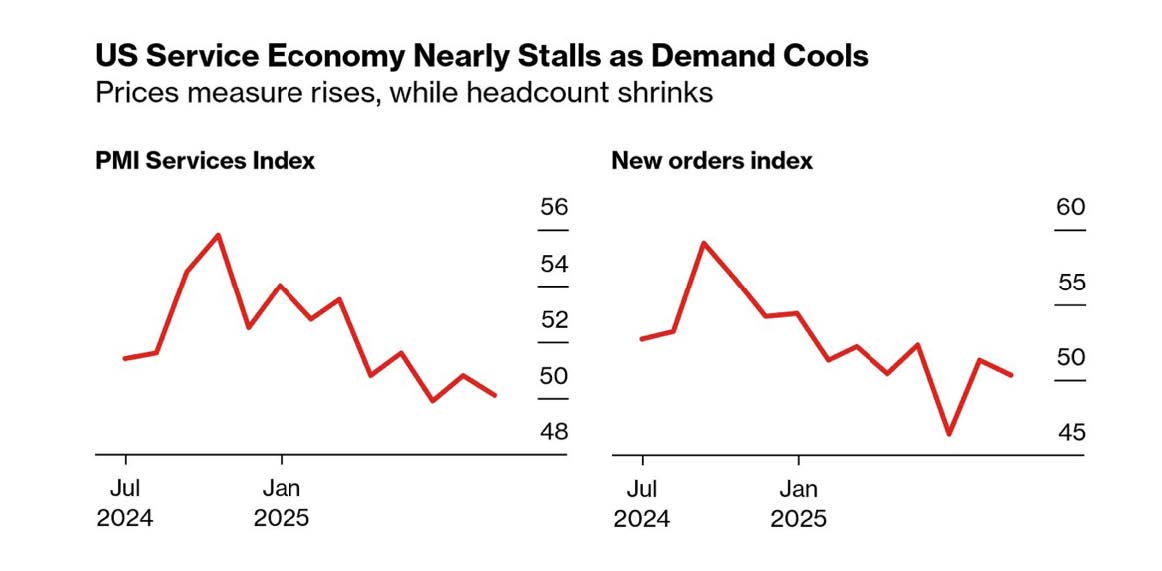

The chart below shows a clear downtrend in a large component of the US economy.

The service sector accounts for close to 70% of the US economy. When the PMI (Purchasing Manager Index) declines as clearly as it has since the beginning of 2025, the economy generally slows.

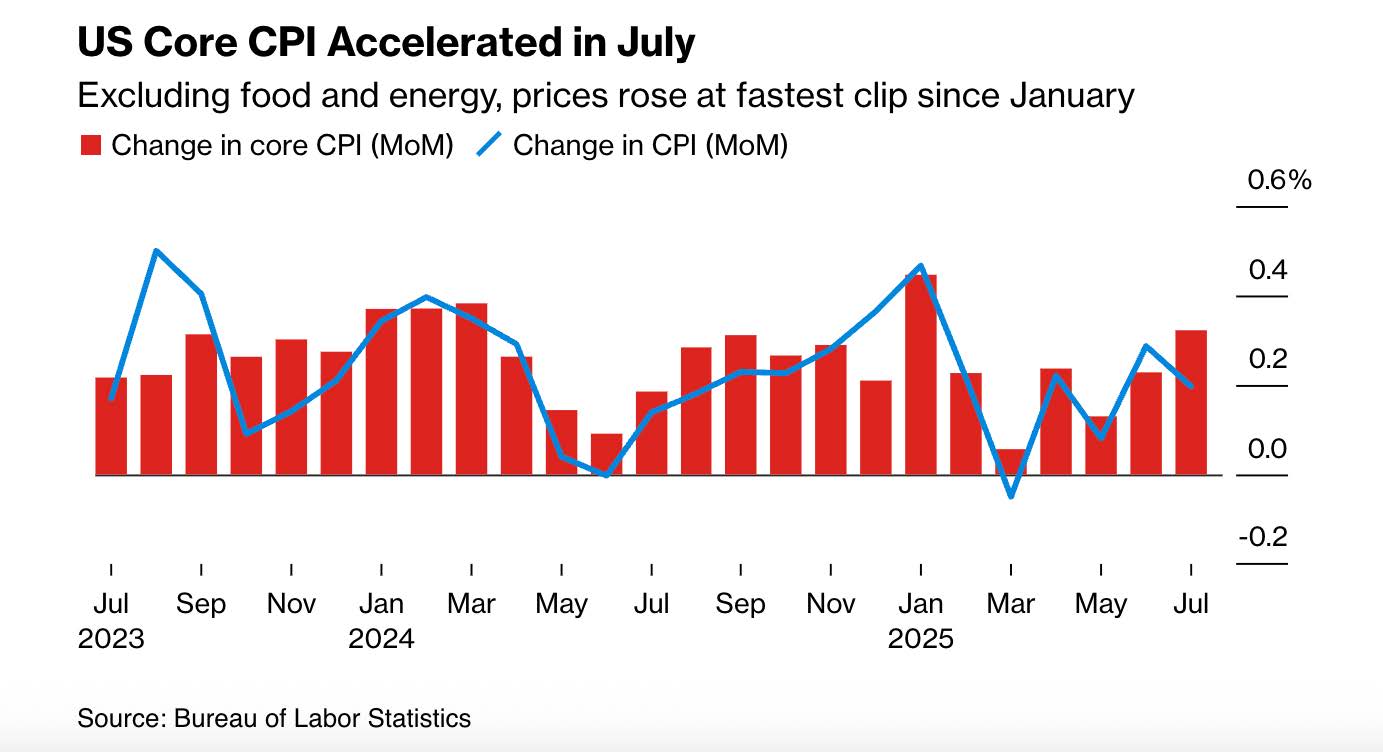

Additionally, when inflation persists, as shown below, prudence is warranted.

We could be entering a period of stagflation. This is an economic environment that we have not seen since the late 70’s and early 80’s.

Portfolio Commentary

During the month of August, I maintained a neutral stance and refrained from adding to our equity positions, in spite of the relentless progression of most equity indices.

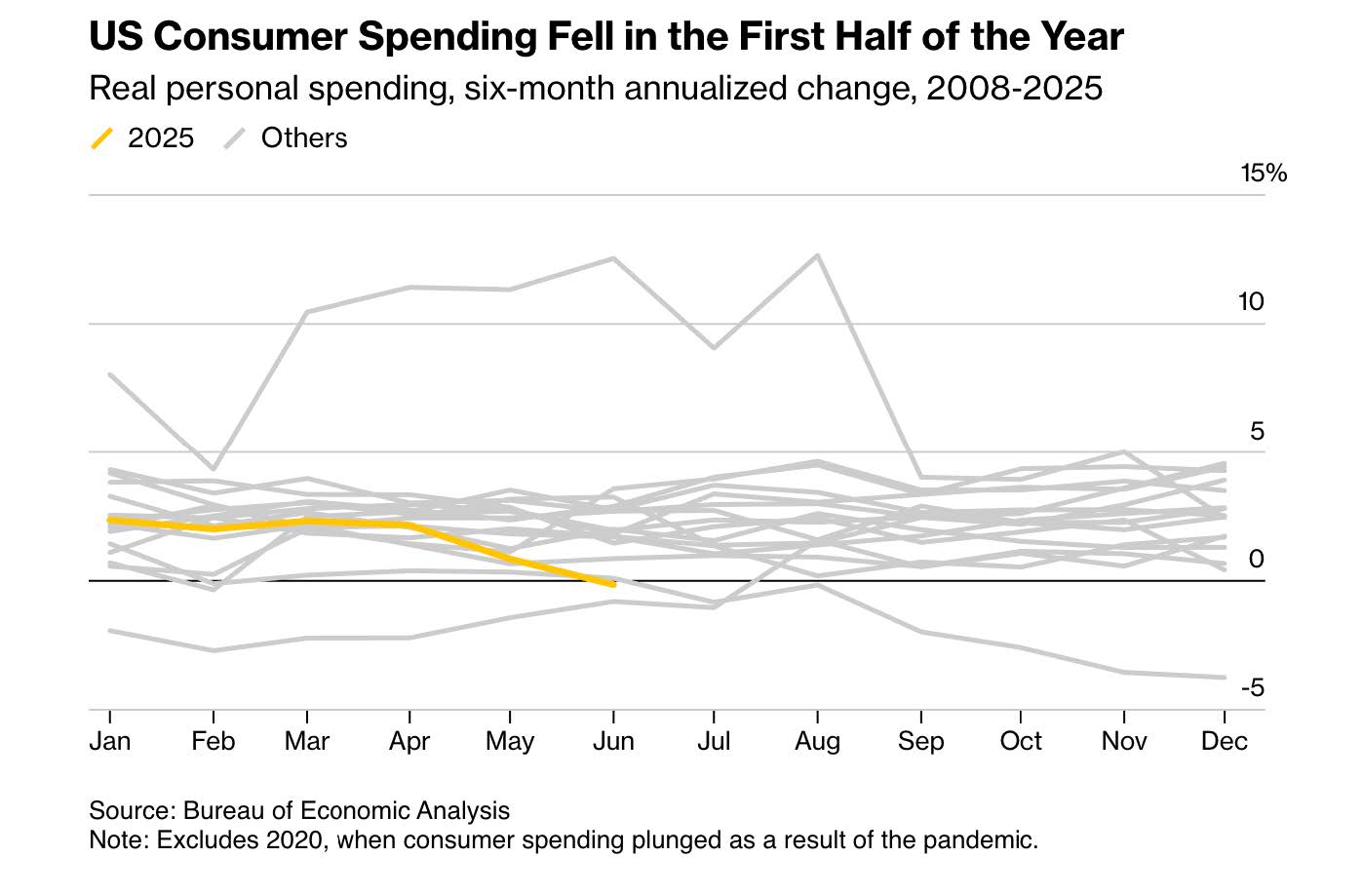

The chart below illustrates well the reason behind my prudent stance.

I do not think much explanation is needed here. The trend (yellow line for 2025) is concerning.

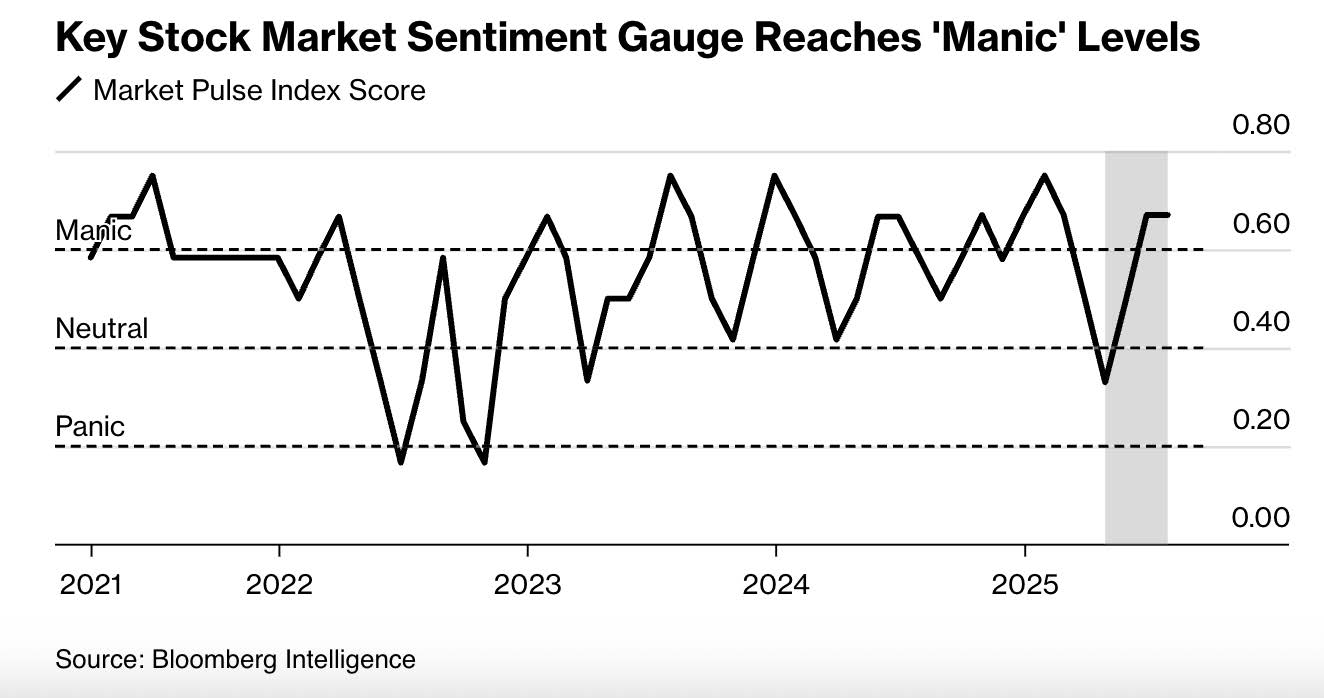

Separately, this likely economic slowdown occurs in an equity environment where overvaluations have been normalized, leading to potentially irrational behavior, as shown below:

While I do not know exactly how Bloomberg constructs this chart, it gives me pause.

Conclusion

My prudent positioning of your accounts since February has led us to lag our benchmark, YTD (year-to-date). While all of them are well in the green this year, I am determined to claw back all or some of our relative under-performance between now and the end of the year.

I think I may get some help from the Trump Administration!

Its relentless attacks on the FED, coupled to its willingness to undermine the credibility of our economic statistics by replacing competent bureaucrats with sycophants, may yet be punished by investors.

Would that be the case, I would be given the opportunity to re-enter the markets at levels that justify more risk-taking.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980