Overview

US equity markets generally declined in February. The S&P 500 lost .76%. The Nasdaq 100 slumped 3.33% while the Russell 2000 (small-cap index) progressed .80%. Internationally, the EPAC BM Index of developed economies (ex-US) rose a robust 5.90%. The MSCI EM (emerging markets) increased 5.51%, while the MSCI Frontier 100 index added 2.86%.

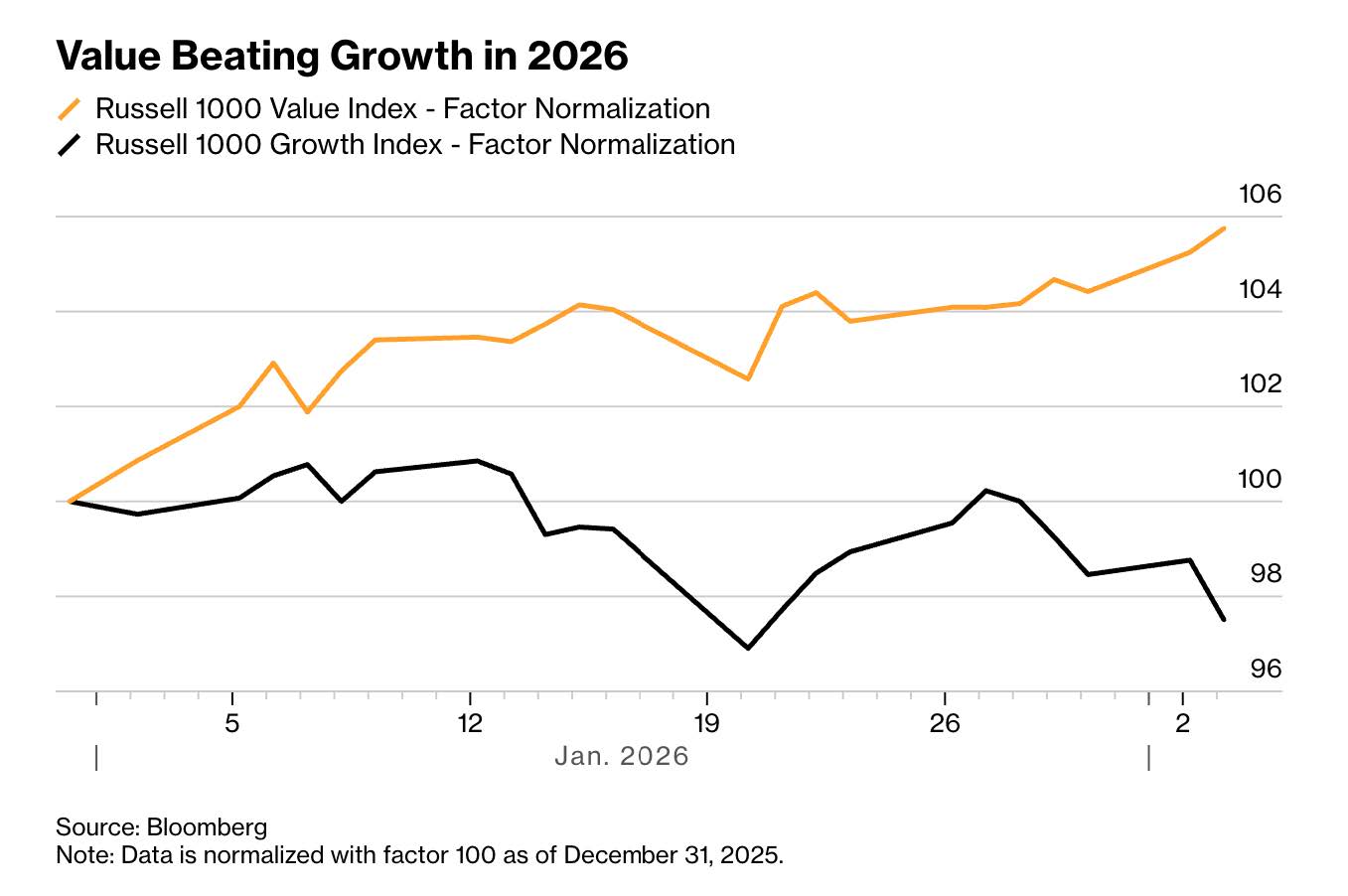

The main reason behind the disappointing performance of US equity indices is the persistent worry that investors have about the sustainability of high stock valuations in the tech sector. The rotation, away from that sector, continued in February, in favor of international equities as well as Small US Caps (Russell 2000) and the Value sector of the US equity market.

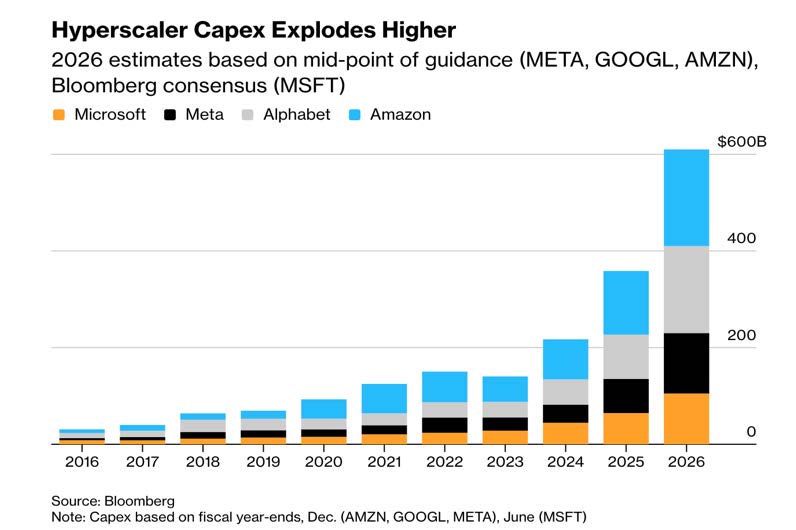

The chart below illustrates the size of the investments made by major tech companies in their race towards AI domination.

Equity investors are worried that the payoff may not ultimately justify the expenses; combined with already high valuations, this explains the sectorial rotation away from tech.

In February, US fixed income markets were up. The US bond aggregate was up 1.64%. Investment-grade corporate bonds gained 1.29%, while high-yield corporates progressed .19%.

Our median portfolio was up 1.96% in January. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 1.45%. Overall, our median portfolio is up 3.97% YTD (Year-To-Date) vs. 3.01% for our benchmark.

Market developments

February was a volatile month for equities. The sectorial rotation that I mentioned earlier in this letter continued, as illustrated below:

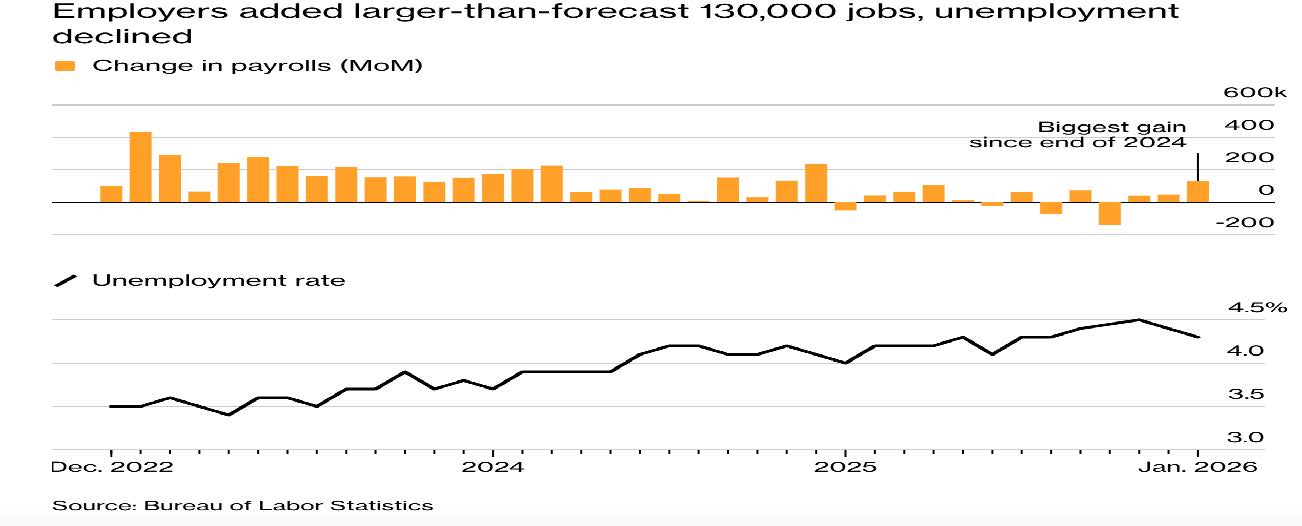

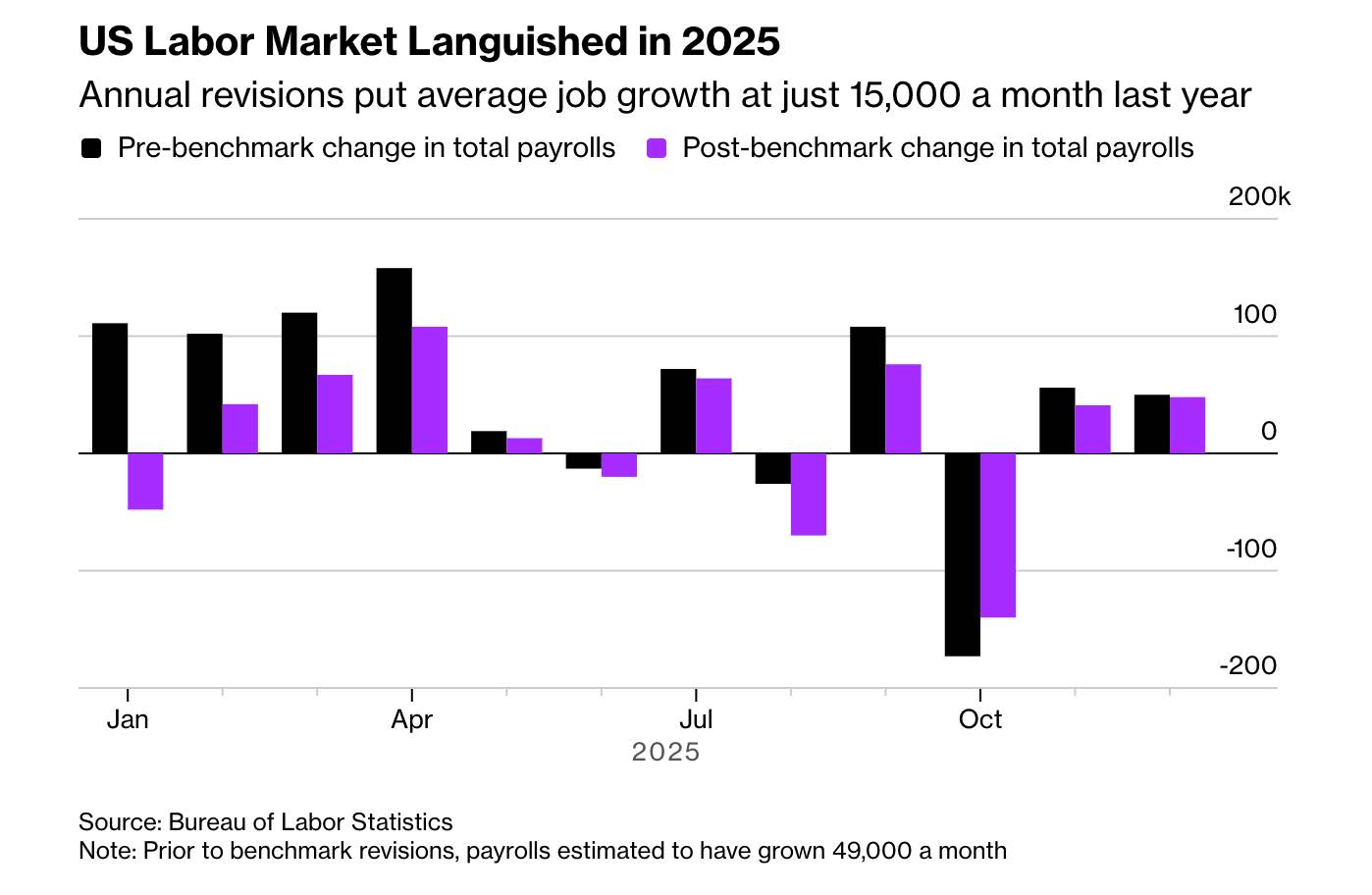

At the same time, economic news on the labor front were mixed while inflation remained higher than wanted by the FED. Below are two charts related to the conditions in the US Labor market. I am not sure what to make of them.

If you believe the above, everything is fine. Then you look at this one and you wonder…

Portfolio Commentary

The mixed message from economic data, the high valuation in the tech sector, the increasing volatility in that part of the equity market AND the violent downdraft experienced by some parts of the equity markets have led me to de-risk most portfolios this month.

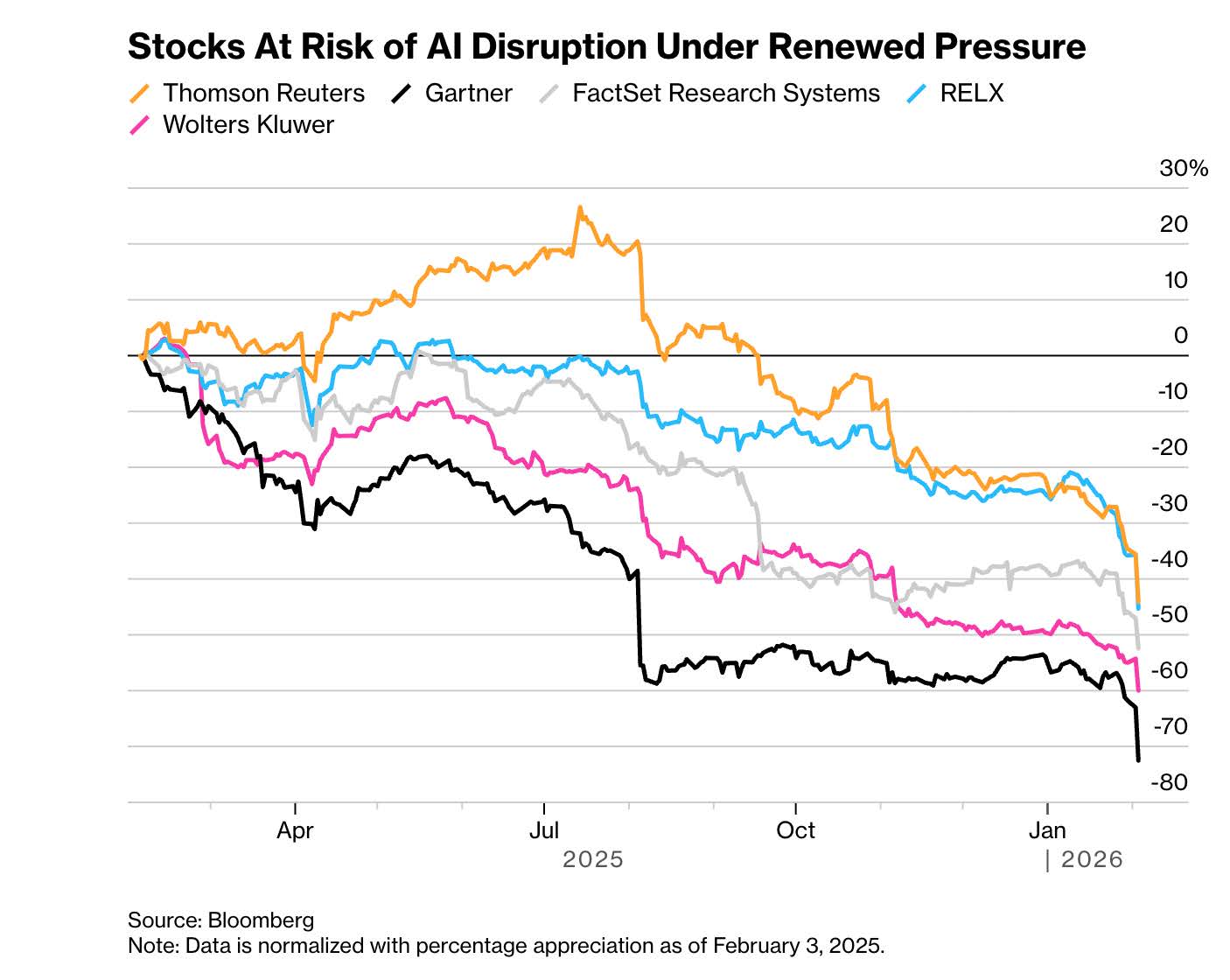

The AI transformation of our economy is starting to inflict pain on some sectors, as illustrated below:

I am not sure that the loss of value of the companies above is warranted, but the conclusion I draw from those drastic moves is that markets are currently beset by very strong undercurrents. In such an environment, it is prudent to reduce risk.

Here is what I have done: 1) I sold 70% of your positions in QQQ (Nasdaq 100 ETF). I did so while minimizing potential capital gains (selling heavily in your qualified accounts), 2) When I could not lighten up QQQ because of the capital gains implications in your taxable accounts, I sold SPY. All in all, this has reduced your exposure to US equities by about 5% to 7% and your exposure to the tech sector by about 80%.

I have used the proceeds from these sales to buy IEFA (international developed non-US equities), VTV (the Value ETF), RSP (the S&P 500 equal weight ETF), and AGG (the US bond aggregate ETF).

These moves have contributed to our good performance this month and have increased our outperformance, YTD.

Conclusion

Last month, I mused about the lack of market reaction to the military strike on Venezuela. Now, as of this writing, the US is striking Iran. This may have more (market) resonance. Oil should be bid up, unless the Iranian regime has lost all potency. It should also keep the price of gold nicely up.

The other development that I am focusing on is the impact of AI on employment going forward. Some firms have already announced severe cutbacks. The long-term effects of this technological revolution on employment are hard to quantify.

That said, a good friend of mine who spent his career in IT believes that the negative implications of AI on youth employment will be devastating. That gives me pause.

All in all, given the short-term military developments and the longer-term implications of AI on unemployment, I am happy to have started to de-risk your portfolios.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980