Overview

The S&P 500 gained 5.26% in May. The Nasdaq 100 jumped 8.43%, while the Russell 2000 (small cap index) rose 4.37%. Internationally, the progression was generally comparable. The EPAC BM Index of developed economies (ex-US) rose 4.73%. The MSCI EM (emerging markets) went up 9.71% but the MSCI Frontier 100 index gained “only” 1.99% as some of its components include countries that were hurt by rising oil prices.

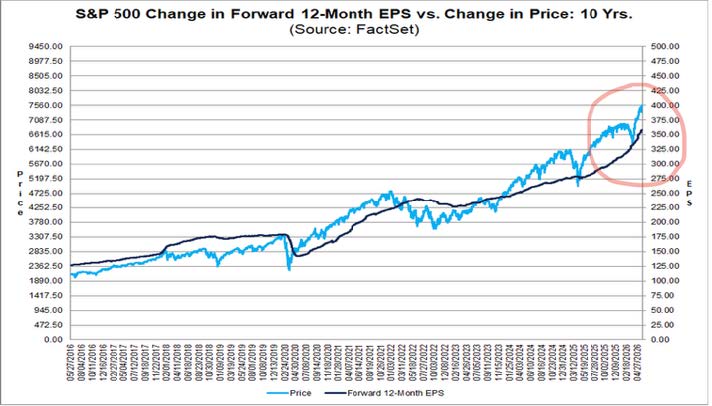

As in April, the rally this past month was driven by the tech sector and underpinned by an acceleration in the growth of corporate earnings, as illustrated in the chart below:

The light blue line represents the price progression of the S&P 500 index. The dark blue line represents the change in forward earnings per share (EPS). Note the steepening of the slope of that line (circled in red). Corporate earnings are increasing sharply as well as growing faster. There has been a clear acceleration (steepening of the curve) over the past 18 months. The steepening appears to be almost entirely due to the exceptional profitability of the tech. sector and by the effect of the AI revolution. This is a remarkably concentrated and, therefore, increasingly dependent market progression.

In May, US fixed income markets were mostly flat. The US bond aggregate gained .31%. Investment grade corporate bonds rose .76%, while high yield corporates returned .49% and the long bond gained .51%.

Our median portfolio was up 1.91% in April. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 2.46%. Overall, our median portfolio is up 4.92% YTD (Year-To-Date) vs. 6.27% for our benchmark.

Market developments

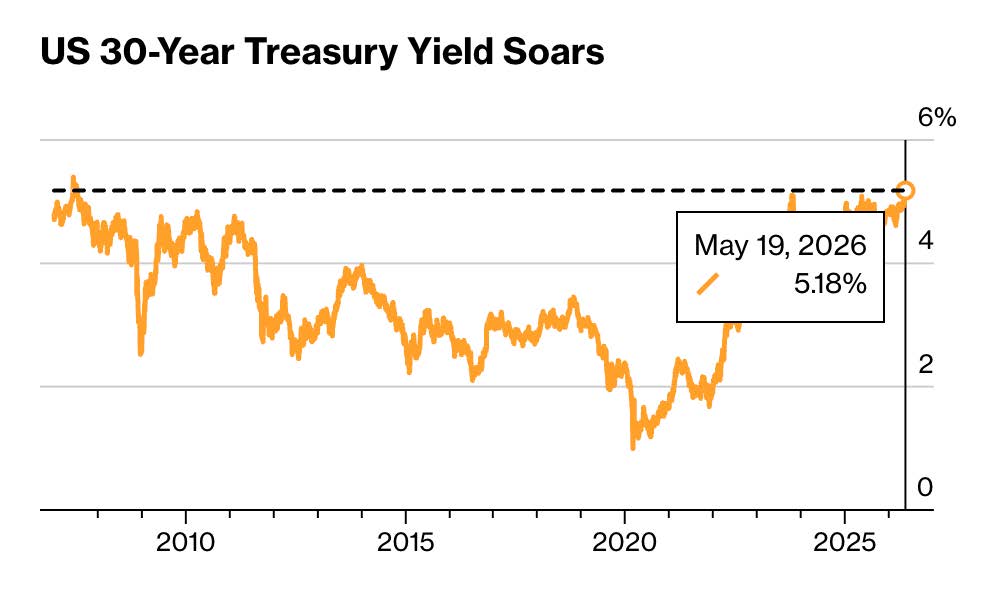

The war with Iran is fueling inflation in the US as well as in the rest of the world. This has caused some ructions in the bond market, as illustrated below:

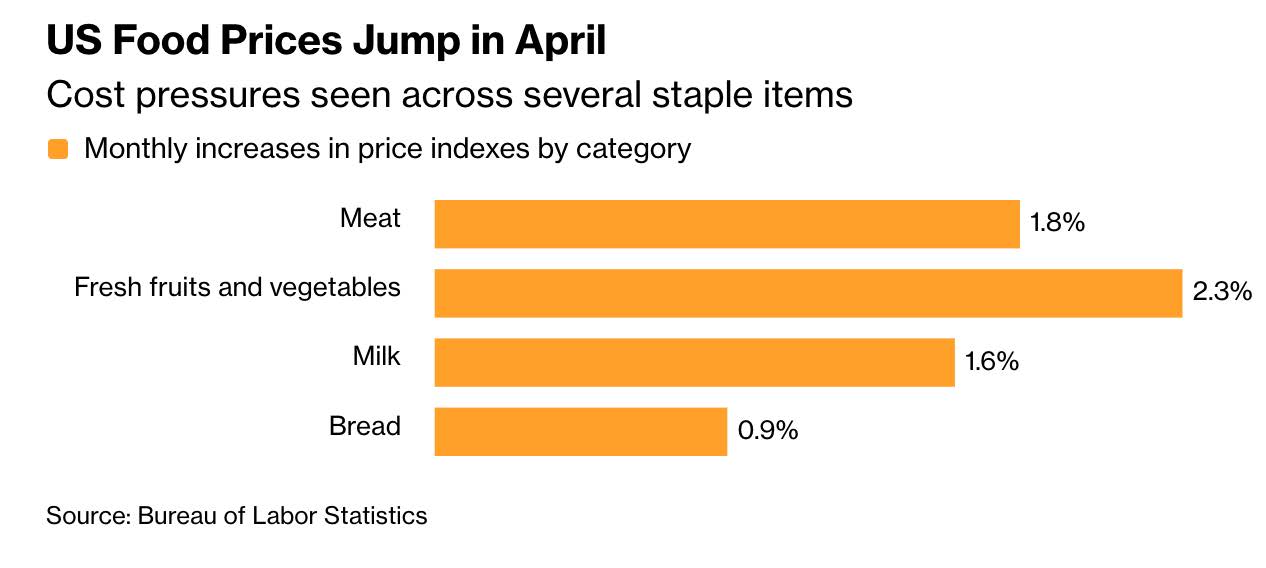

Long-term rates have risen in the first part of the month of May as fears that inflation would be staying with us longer than anticipated took hold. Those fears were somewhat calmed during the second part of May as signs of a slowing economy countered the inflationary narrative. Most significant among them were the consumer confidence numbers that showed that the average American consumer is tired and depressed. Bond investors think that this situation, at some point, will cause the Federal Reserve to push interest rates down again and that inflation will not endure. For now though, prices are up and significantly so, as illustrated in the chart below:

Oil prices are not helping either. An end to the conflict with Iran should offer some relief. The proximity of US elections might bring about a resolution over the summer.

Portfolio Commentary

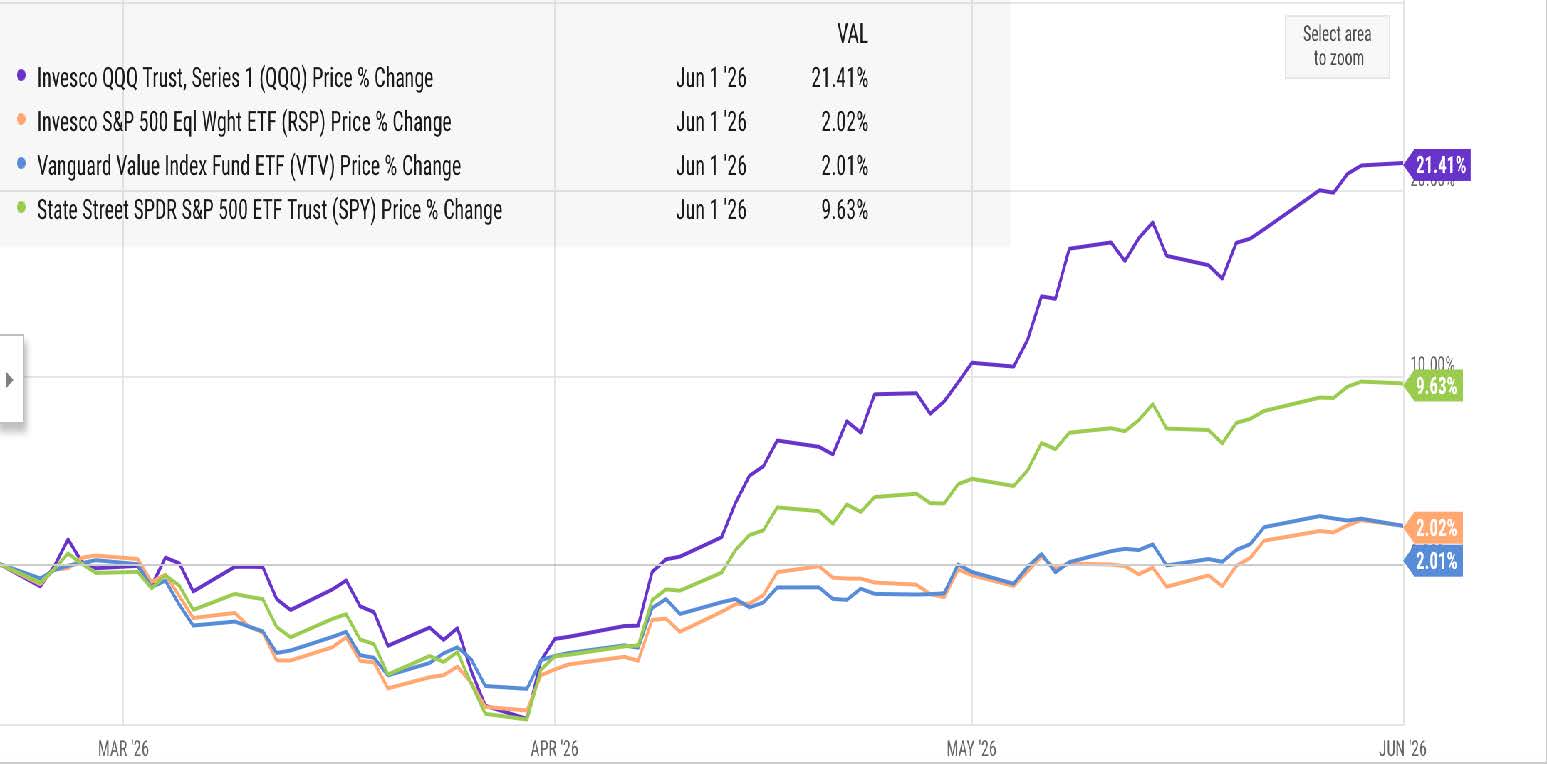

In May, the sectorial rotation in favor of the tech sector continued unabated.

It can be illustrated below by the discrepancies in performance between several sectorial ETFs.

Since the beginning of the war with Iran, around February 20, the tech sector (purple line) is up 21%. Over the same period an equal weighted version of the S&Ps’500 is up a mere 2% (orange line). The same is true for the value sector (blue line). The S&P 500 itself (green line) is right in the middle at about 9%, performance-wise, over the period. This is because about 45% of its capitalization results from seven mega tech stocks.

The concentration risk is real, but it makes everyone who does not believe that this run up in price is eternal, look bad in comparison. At some point the market will correct and when that happens, the tech sector is likely to take the brunt of the drawdown.

This reality has caused me to proceed carefully. In May, I reinvested part of the proceeds from maturing US Treasuries in your portfolio in QQQ. We are still underweight the tech sector by a significant margin. This could cost us should the rally endure.

That said, with a 25% performance since the beginning of the conflict with Iran, a tired US consumer and with growing inflationary pressures, I doubt that the tech rally will continue to defy gravity for much longer.

Conclusion

Economic clouds are accumulating.

Inflation is pushing the average US consumer to pile on credit card debt and/or restrict herself. The Iran conflict continues causing the world economy to gradually slowdown and putting pressure on bond yields as governments around the world borrow more to support their economies.

Geopolitically, the rule of law is receding in the West and, regrettably, powerfully so in the US. The long-term implications of this degradation of political and economic norms are hard to measure but will become increasingly apparent if we continue to fail to fight it.

Its effects on stock markets, here and around the world, may not be forever mundane.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980