Overview

The Middle East war started by Israel and the US against the Iranian regime, at the end of February, upended markets in March.

The S&P 500 lost 4.98%. The Nasdaq 100 slumped 4.68% while the Russell 2000 (small cap index) declined 5.00%. Internationally, the damage was worse due to the rise of the USD and the sharper consequences of rising oil prices on more dependent economies. The EPAC BM Index of developed economies (ex-US) sunk 12.98%. The MSCI EM (emerging markets) declined 13.03% while the MSCI Frontier 100 index dropped “only” 8.16% as some of its components include countries that benefit from rising oil prices.

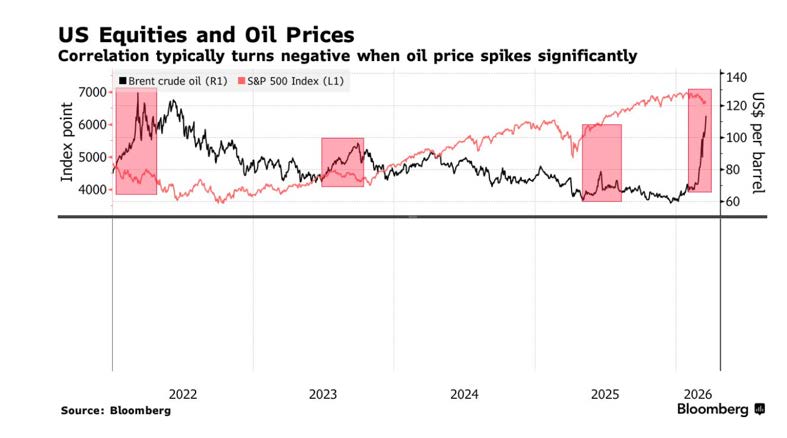

The chart below illustrates well the negative correlation between rising oil prices and their impact on US equity valuations:

It is unlikely that equity markets will resist a serious correction if the Strait of Hormuz is kept closed much longer. The consequences of this situation are also palpable in the bond market where yields have risen measurably. The chance of the Federal Reserve reducing the Fed Funds Rate anytime soon is now nil and long-term yields have adjusted in response (up .30% for the long bond).

In March, US fixed income markets were down. The US bond aggregate lost 1.76%. Investment grade corporate bonds declined 1.98%, while high yield corporates lost 1.18%.

Our median portfolio was down 3.95% that month. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) lost 3.95%. Overall, our median portfolio is down .32% YTD (Year-To-Date) vs. 1.09% for our benchmark.

Market developments

The war with Iran has dominated the market narrative this past month and is likely to continue to do so until a cease fire is achieved. Its consequences for the US economy are already palpable with rising prices at the pump, lower consumer confidence and expectations of a higher level of inflation going forward.

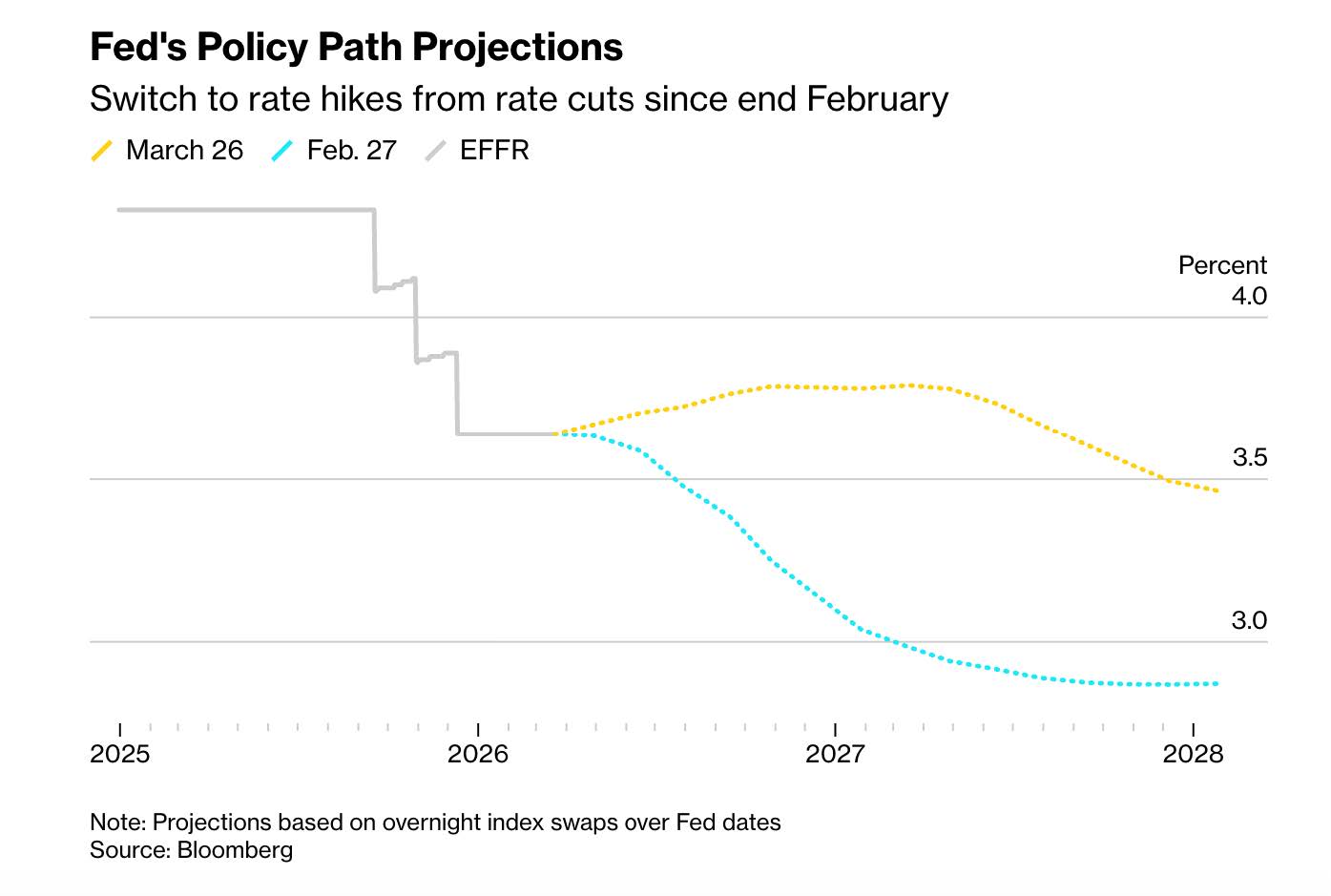

The chart below illustrates how market expectations of Fed funds rate cuts have been altered since the beginning of the conflict:

At the beginning of the year, expectations of cumulative rate cuts of .75% through 2028 (light blue line) were “priced in”. In other word, this is what the market expected and had priced equities on.

With only a third of those cuts now expected over that period, and only at the very end, the support that rate cuts generally provide to equities will be muted.

That support could turn into headwinds very quickly if the war with Iran were to last significantly longer than the “four to six weeks at most” promised by President Trump. This would cause inflationary pressures to become potentially “anchored” in most economic actors’ minds (consumers, investors etc…) increasing in the process the chances of a higher level of inflation for a longer time. None of this would be good for the economy and the stock market.

Portfolio Commentary

In March, with oil prices and interest rates rising, stock prices dropping and the White House sending contradictory messages within days of each utterance, I felt a marginal reduction in risk level was warranted.

Wherever I could and without generating additional capital gain liabilities, I sold SPY, the S&Ps 500 ETF and/or IEFA, the ETF that exposes us to the international developed markets. These sales were relatively modest, representing at most 3% of your portfolios. I declined to sell more given the uncertainty of the current environment and the likelihood of a sharp move up should the White House decide to end the conflict.

While our international equity investments suffered in March, they only gave up the advance they had taken over their US brethren before the start of the war.

As a consequence, most of your portfolios are where they were at the beginning of the year or within less than 1% of that mark.

There might be some investment opportunities for us as the war continues. I say so with mixed feelings about it, of course.

Below is a chart of the Nasdaq 100:

The drop in valuation in that sector since the beginning of the year has accelerated with the Iranian conflict. I may consider allocating more to it should the situation stabilize a bit.

Conclusion

Clearly, Iran is not Venezuela. The US Administration has miscalculated. Their ability to control the situation seems to be, at best, tenuous. I am not sure where that leaves us from an investment point of view.

On the one hand, the US President seems to have a low tolerance for equity losses. If that continues to be the case, a significant correction is not immediately likely.

On the other hand, the problem with oil prices is that they affect more than just what the US President has control over. For the situation to improve, or not deteriorate further, the Strait of Hormuz needs to be reopened quickly. If that is not achieved, a serious correction might eventually take place.

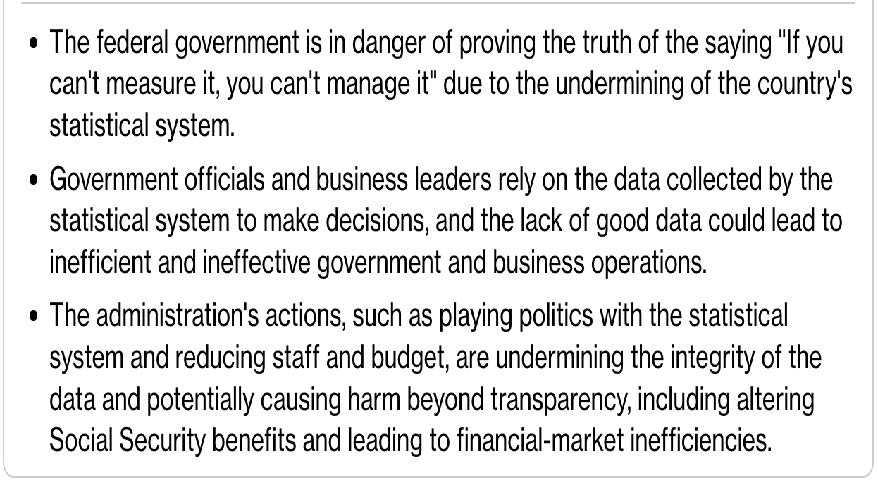

I will conclude this letter with another concern that I have had for a while now. I am worried about what the current administration is doing with the agencies that are responsible for calculating and disseminating the economic data that I, and all market participants, use to base their economic decisions on. Clearly, I am not the only person worried about this.

Below are a few paragraphs taken from an opinion piece written by Michael Bloomberg a few days ago.

I hope to be able to conclude the next newsletter in early May on a more positive note.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980