Overview

US equity markets rose in January but in an uneven fashion. The S&P 500 added 1.45%. The Nasdaq 100 gained .95% while the Russell 2000 (small-cap index) progressed a whopping 5.35%. Internationally, the EPAC BM Index of developed economies (ex-US) rose a robust 6.10%. The MSCI EM (emerging markets) increased 8.86%, while the MSCI Frontier 100 index added 8.76%.

The main reasons behind those significantly divergent performances in favor of the international sector and of small US capitalization stocks, among other sectors, are a relative sectorial rotation away from US large caps, a decline of the USD, and an acceleration of the “debasement” trade. The “debasement” trade generally refers to a repositioning of assets by investors to mitigate the effects of large fiscal deficits and the decline of fiat-currency (the USD) due to money-printing policies.

The relative move away from US large-cap and tech stocks by a variety of investors results from the policies of the US Administration. Those policies (tariffs, threats of attacks on NATO allies, attacks on the independence of the Federal Reserve, and an inability or unwillingness to seriously address fiscal deficits) all tend to weaken the USD and increase market uncertainties. In that context, it is logical that investors would move to reduce risk by divesting from those sectors that have propelled US stocks over the past three years (large-cap tech stocks) and that are the most susceptible to a correction.

The chart below illustrates partially this situation:

Since October 2025, the Nasdaq 100 index has not progressed.

In January, US fixed income markets were marginally up. The US bond aggregate was up .11%. Investment grade corporate bonds gained .18%, while high yield corporates progressed .51%.

Our median portfolio was up 1.94% in January. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 1.54%.

Market developments

The equanimity of US equity investors is simply remarkable.

A military strike on Venezuela, the killing of two Minneapolis protestors by ICE and the prosecution of Fed Chair Jerome Powell by the Justice Department, all unexpected or unprecedented actions and events that are in many ways perpetrated in defiance of the rule of law, have not had a meaningful impact on US markets.

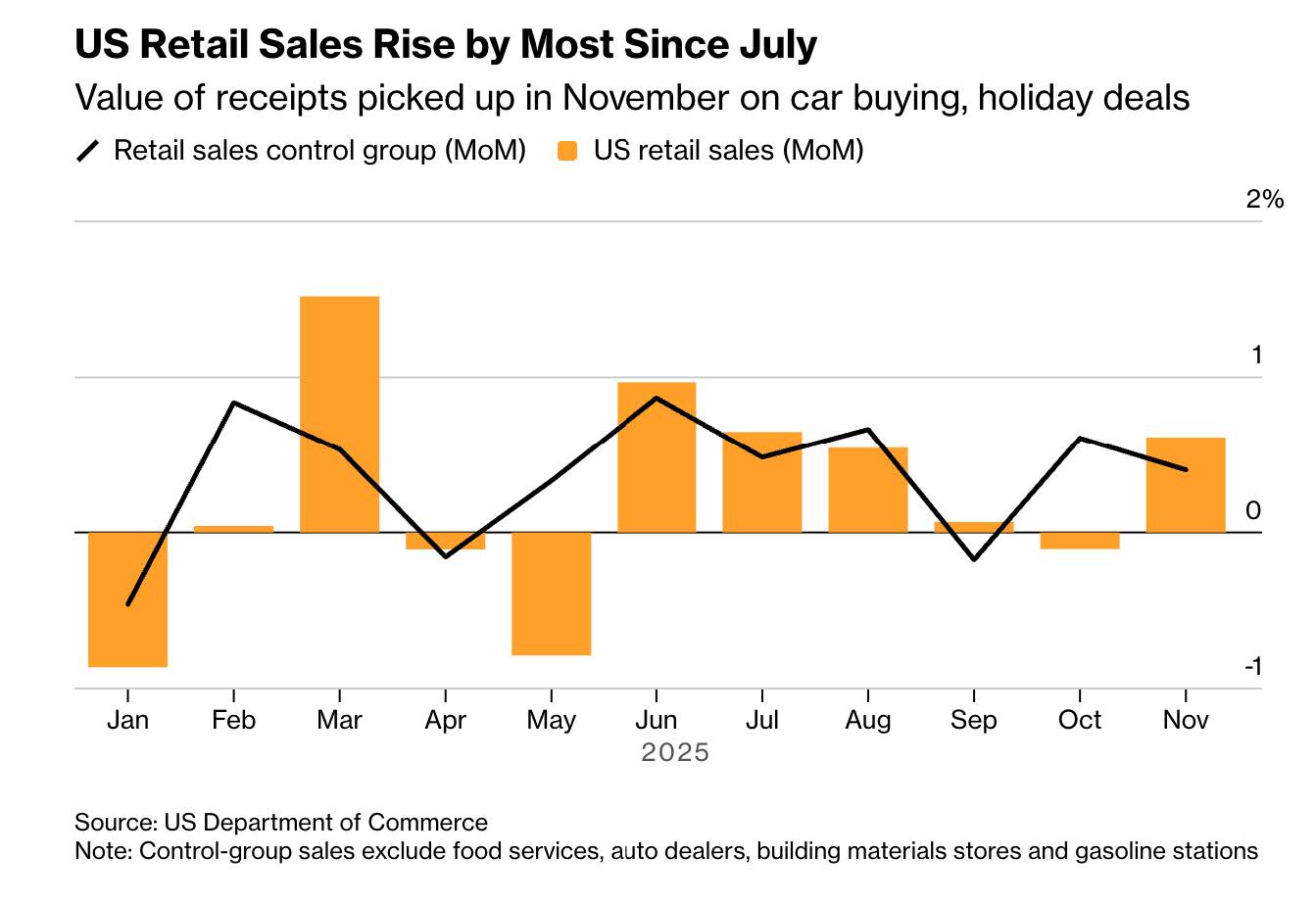

The US economy seems to be chugging along, seemingly unresponsive to this environment, as illustrated by recent retail sales numbers below:

Additionally, fourth-quarter corporate earnings have so far come in above expectations and supported valuations.

All in all, other than for the “debasement” trade discussed above, which clearly indicates that something is amiss or changing, all seems well in the US of A, as far as equity investors are concerned.

I am quite satisfied with that as a money manager, but I also wonder how long the disregard for the rule of law, the US Constitution, and the institutions that support it by the current administration can continue without impacting markets more seriously.

Portfolio Commentary

This past month, I partially divested from Air Liquide (AIQUF) in favor of our international developed markets ETF (IEFA). Going forward, I intend to continue with this move away from AIQUF and into IEFA. This stock has stagnated since October, and I do not see a mediumterm catalyst for a change.

Our investment in IAU (the gold ETF) progressed another 12% in January, in spite of a serious drop of 10% in the last two days of the month. I intend to take some profits going forward. On average, depending on the timing of my initial purchase for each portfolio, our investments in IAU have netted gains of 35% since September 2025 (the time of my last purchase), up to 80% for accounts that benefited from my initial investments in 2023 and 2024.

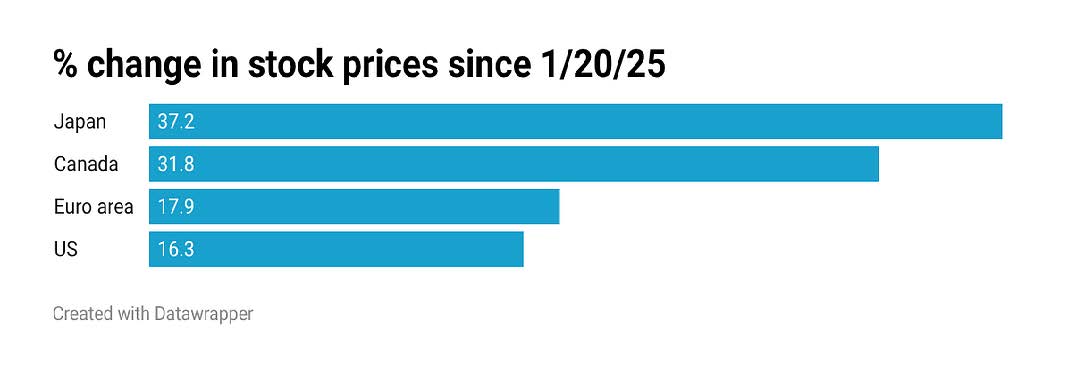

Looking ahead, I am satisfied with the way your portfolios are currently positioned. About half of our US equity investments are in sectors that are fairly valued (VTV), and we have a meaningful exposure to international developed equities that have performed well, as shown below:

The performance numbers above exclude the effects of the decline of the USD currency.

With respect to the large-cap/tech sector in the US, I intend to maintain our relatively prudent allocation despite its high valuation.

Earnings in the sector remain supportive, and I do not yet see a catalyst for a correction despite the punishing declines that can affect individual stocks when their outlook disappoints investors, as was the case for Microsoft this past week.

Conclusion

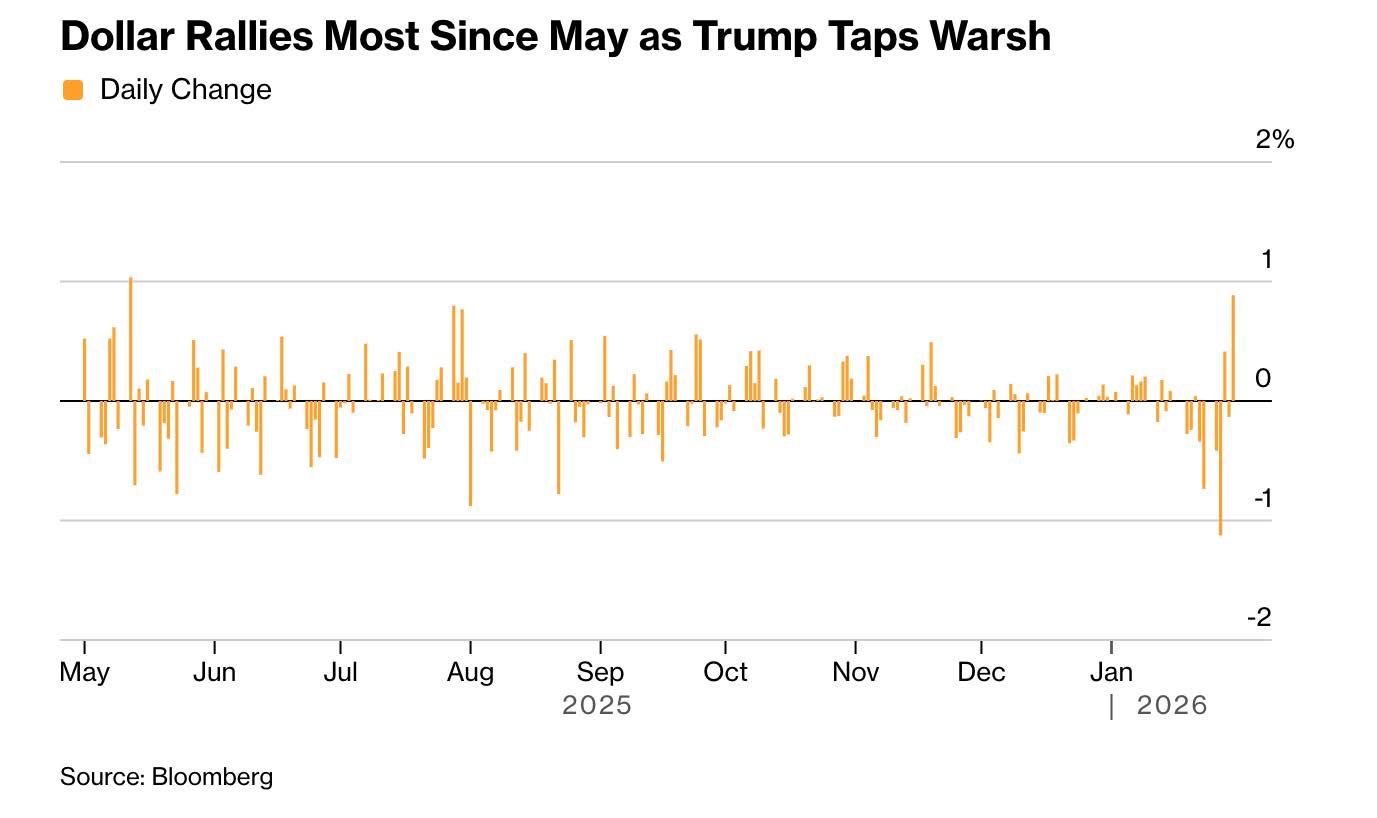

On Friday, President Trump announced that Kevin Warsh will replace Fed Chair Powell in May 2026, when the latter’s term expires.

The announcement has provided some comfort to market participants. Mr. Warsh is viewed as a knowledgeable professional who, in the past, has fiercely defended the independence of the Federal Reserve and supported rather hawkish policies.

His nomination has boosted the USD, as illustrated below:

Also, it has caused a severe drop in the price of gold.

However, President Trump has demonstrated a preference in surrounding himself with sycophants. Whether Warsh fits this profile and can resist the president’s assaults on the Fed’s independence will have meaningful consequences on the course of economic policy and markets.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980