Overview

The fragile ceasefire in the conflict opposing the USA and Iran in the early part of April has caused equity markets to jump powerfully since.

The S&P 500 gained 10.49% in April. The Nasdaq 100 jumped 15.31%, while the Russell 2000 (small-cap index) rose 12.21%. Internationally, the progression was generally less exuberant. The EPAC BM Index of developed economies (ex-US) rose 9.03%. The MSCI EM (emerging markets) went up 14.73%, but the MSCI Frontier 100 index “only” 5.93%, as some of its components include countries that were hurt by rising oil prices.

The spectacular market performances in April were in part the consequence of the cessation of openly destructive military operations. However, the surprisingly good first-quarter corporate earnings provided the fuel and the accelerant that kept equities going towards one of their best monthly performances in years.

The chart below illustrates this point eloquently:

At the end of April, 80% of the S&P 500 corporations that had reported their first-quarter earnings had beaten expectations, sometimes in spectacular fashion, particularly in the Tech sector.

In April, US fixed income markets were mostly flat. The US bond aggregate gained .11%. Investment-grade corporate bonds rose .45%, while high-yield corporates returned 1.69%, and the long bond declined .69%.

Our median portfolio was up 3.35% in April. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 4.84%. Overall, our median portfolio is up 3.06% YTD (Year-To-Date) vs. 3.65% for our benchmark.

Market developments

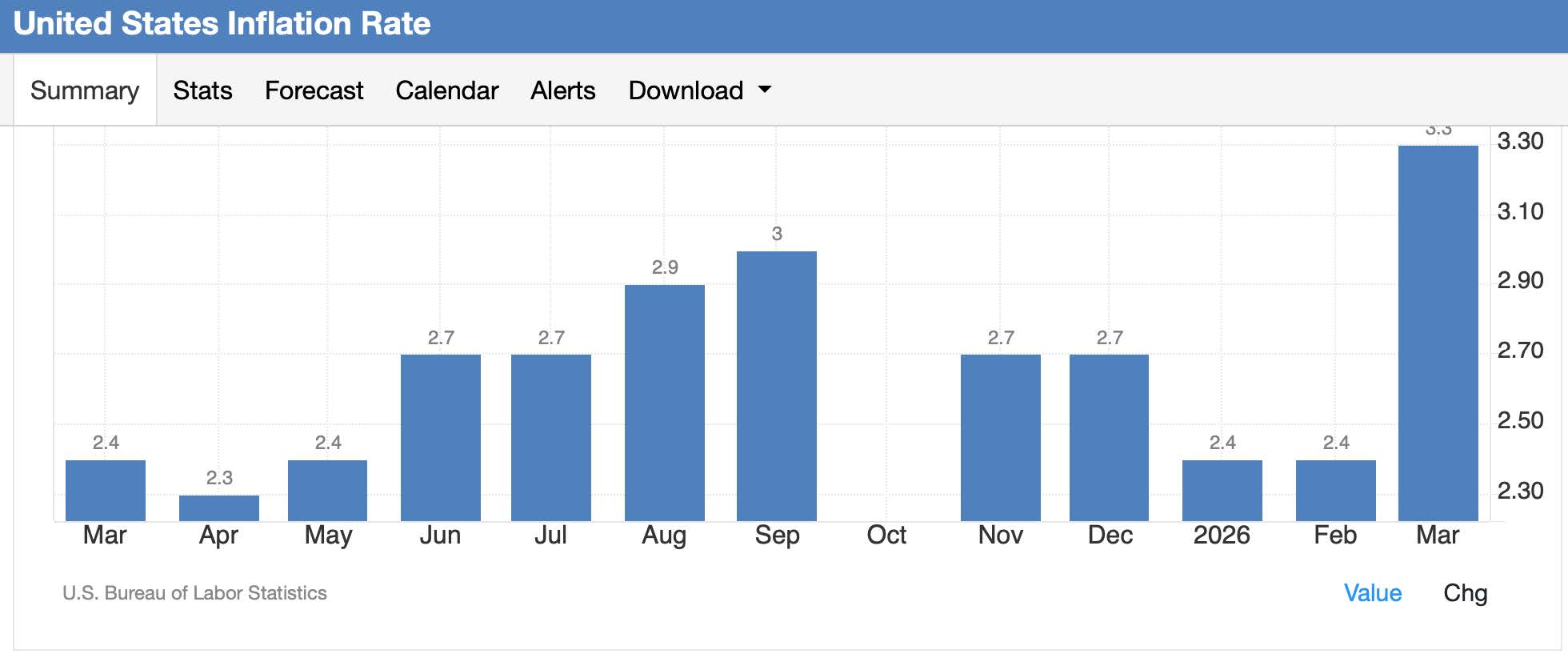

The economic data released during the month of April generally showed that the American economy remains surprisingly robust. Inflation is on the rise, undoubtedly, in part the result of the misguided tariff policies of the current Administration and in part as a corollary to the war with Iran, as shown below:

On the other hand, large item (capital goods) investments remain elevated as shown below:

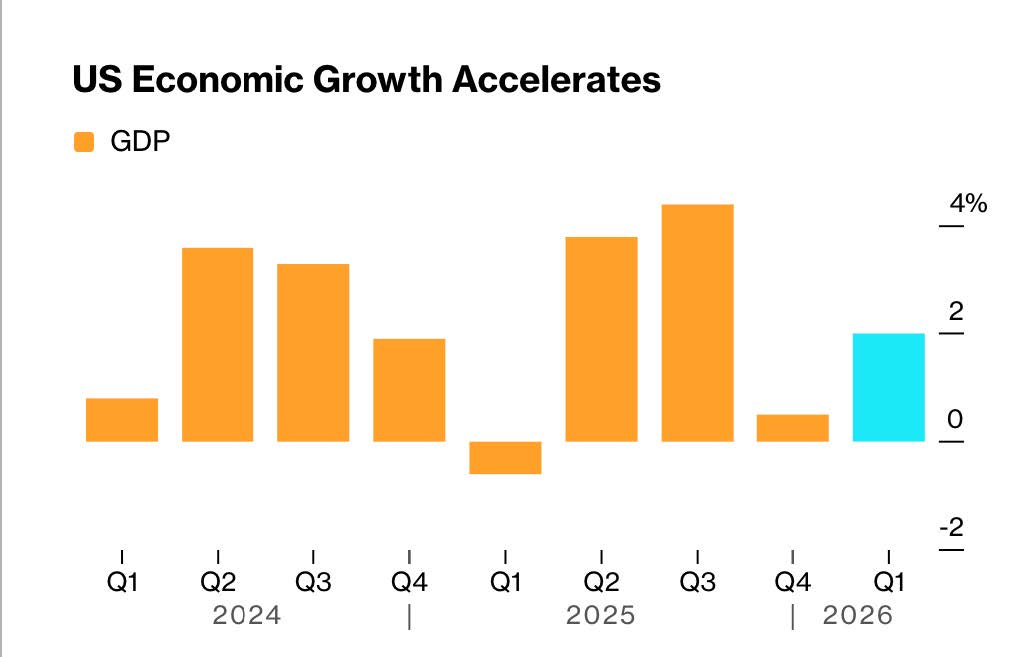

And, GDP growth for the first quarter is still solid, if a tad below expectations:

The American economy appears to be propped up by the huge investments associated with the build-up of its AI infrastructure. More on this in our next section.

Portfolio Commentary

April saw the return of the sectorial rotation in favor of the Tech sector, generally, at the expense of the rest of the market. From October 2025 until the end of March 2026, this sectorial rotation had stopped or reversed in favor of US value and international stocks. The announcement of the cease fire in the Middle East conflict coupled to strong earnings and investment trends coming from the hyper scalers, especially, convinced investors that it was time to resume buying the sector again.

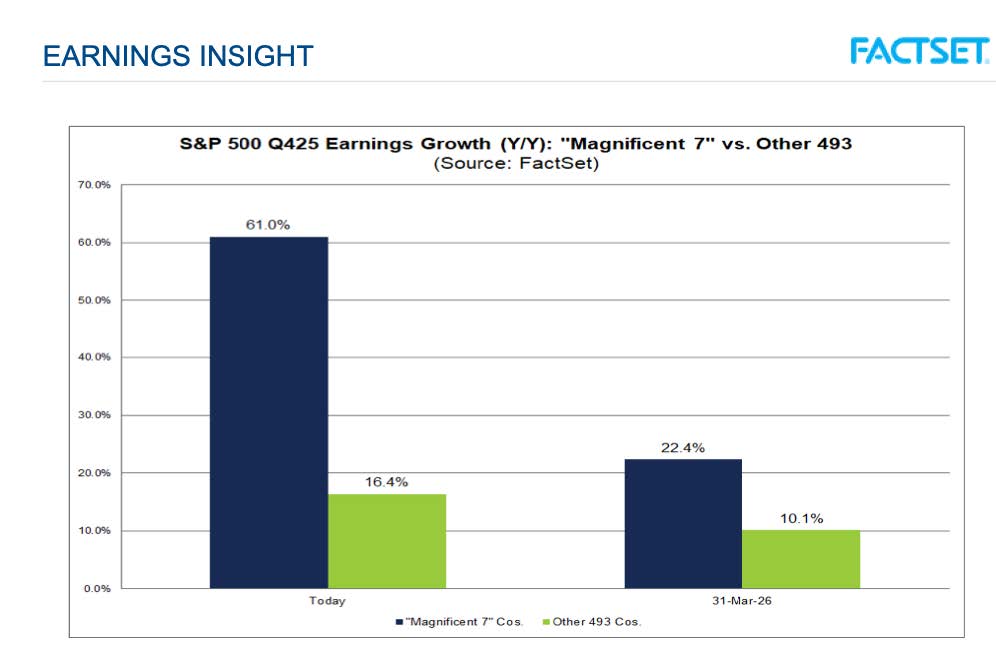

The graph below shows the acceleration in earnings growth for the mega capitalization stocks (Magnificent Seven) in the Tech sector:

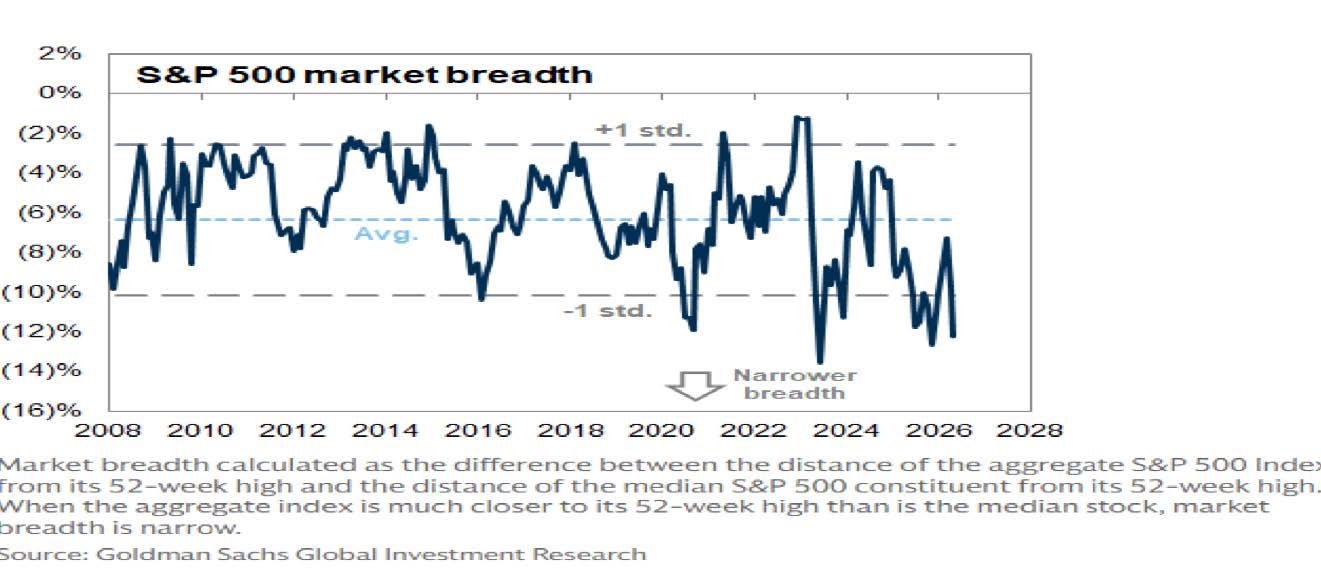

So far, their gargantuan investment in their AI infrastructure has not reduced their profitability, on the contrary. Investors believe that this is set to continue despite the narrowness of this advance, when compared to the rest of the US equity market, as illustrated in the chart below:

What this graph illustrates is that the performance of US equity indices is increasingly dependent on a very limited number of corporate actors.

If diversification reduces risk, then concentration might increase it. Would it not?

Conclusion

While our median performance in April was positive, it did not reach the level that we would have expected in such a rising environment. The reasons for it are principally that: 1) We remain under-allocated to the Tech sector, 2) Our international investments (IEFA in particular) underperformed due to the impact of rising oil prices on Asian and European economies.

I expect the relatively negative trend pushing against international equities to reverse over the coming weeks, particularly if the conflict in the Middle East is resolved satisfactorily (a tall order given the current stalemate).

As for our allocation to the Tech sector, I intend to increase it as our US Treasury holdings mature and cash is freed. Given the relatively high valuations in that sector and the concentration risk discussed earlier in this letter, a measured approach seems appropriate.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980