Overview

US equity markets meandered throughout the month of November, oscillating between slightly positive performances and a small drawdown in the tech/growth sector. The S&P 500 added .25%. The Nasdaq 100 lost 1.45%. The Russell 2000 (small-cap index) was up .96%.

Internationally, the EPAC BM Index of developed economies (ex-US) rose .58%. Emerging markets were mixed. The MSCI EM (emerging markets) dropped 2.38% while the MSCI Frontier 100 index added 1.40%.

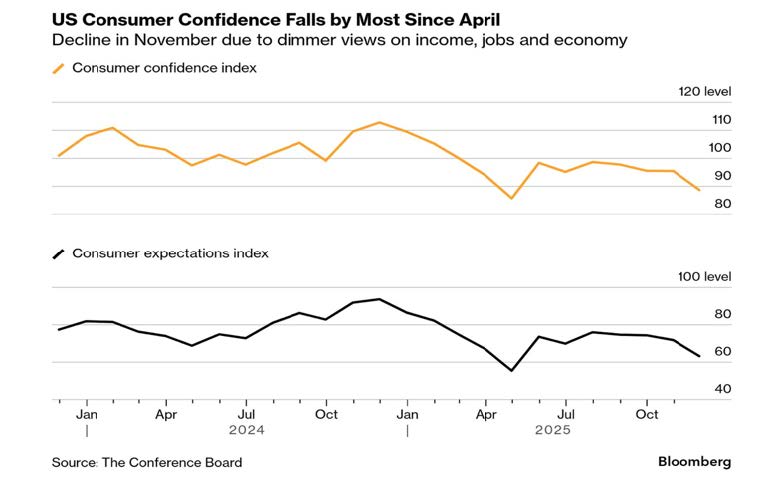

The contradictory signals sent by the US economy, at a time of meager data releases due to the government shutdown, explain in part the contrasted performances. While good third-quarter corporate earnings continued to provide a solid base for US equities, signs of an economic slowdown lingered, as shown below with the graph of US Consumer Confidence:

In November, US fixed-income markets progressed. The US bond aggregate was up .62%. Investment-grade and high-yield corporate bonds gained .65% and .58% respectively.

Our median portfolio was up .68%. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose .12%. Year-to-date (YTD), our median portfolio is up 9.01% vs. 14.41% for our benchmark.

Market developments

Signs of market froth have been long visible in US equity markets, but had been of little import to US investors until early November. Only then did worries about excessive valuations in the tech sector express themselves through a market drop of close to 4%. The main trigger behind the drop was a change in investors’ perception of the FED’s intentions.

Early in November, market expectations of an interest rate cut at the FED’s December meetings faded. Signs of persistent inflation seemed to overtake employment and consumption concerns. This caused a reassessment of the FED’s intentions. The market dropped. This did not last long.

US equity markets have gone up and down in November, together with the changing probabilities of a FED interest rate cut. As probabilities faded from 80% early in early November to 50% in the middle of the month, markets dropped. As probabilities increased again to about 80%, where they currently stand, markets resumed their uptrend.

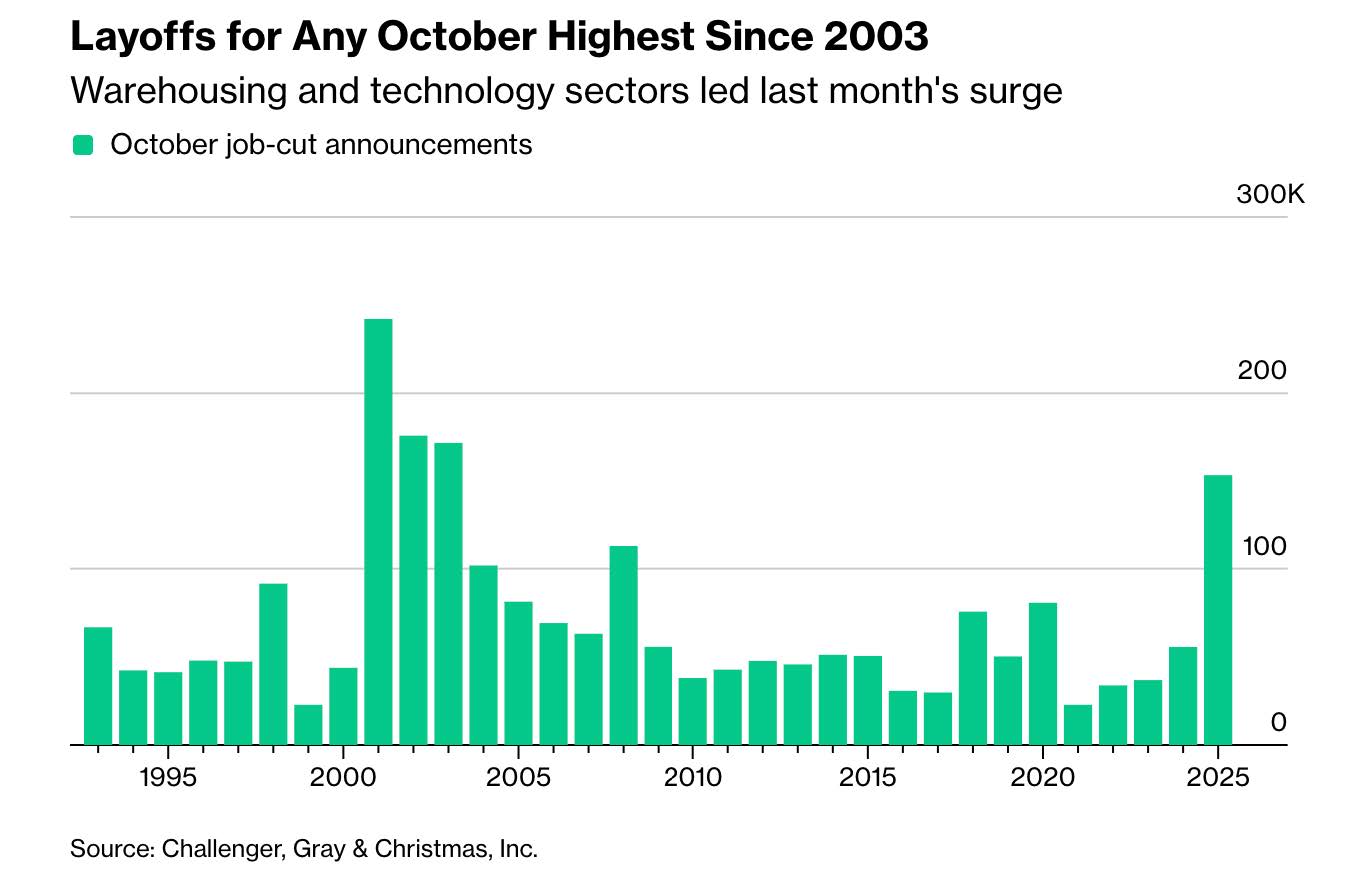

At this juncture, the FED’s conundrum is real. Should they provide more liquidity (reduce interest rates a bit more) to support consumption and rising unemployment, as illustrated below:

or should they tighten to further reduce inflation? The jury is out.

Portfolio Commentary

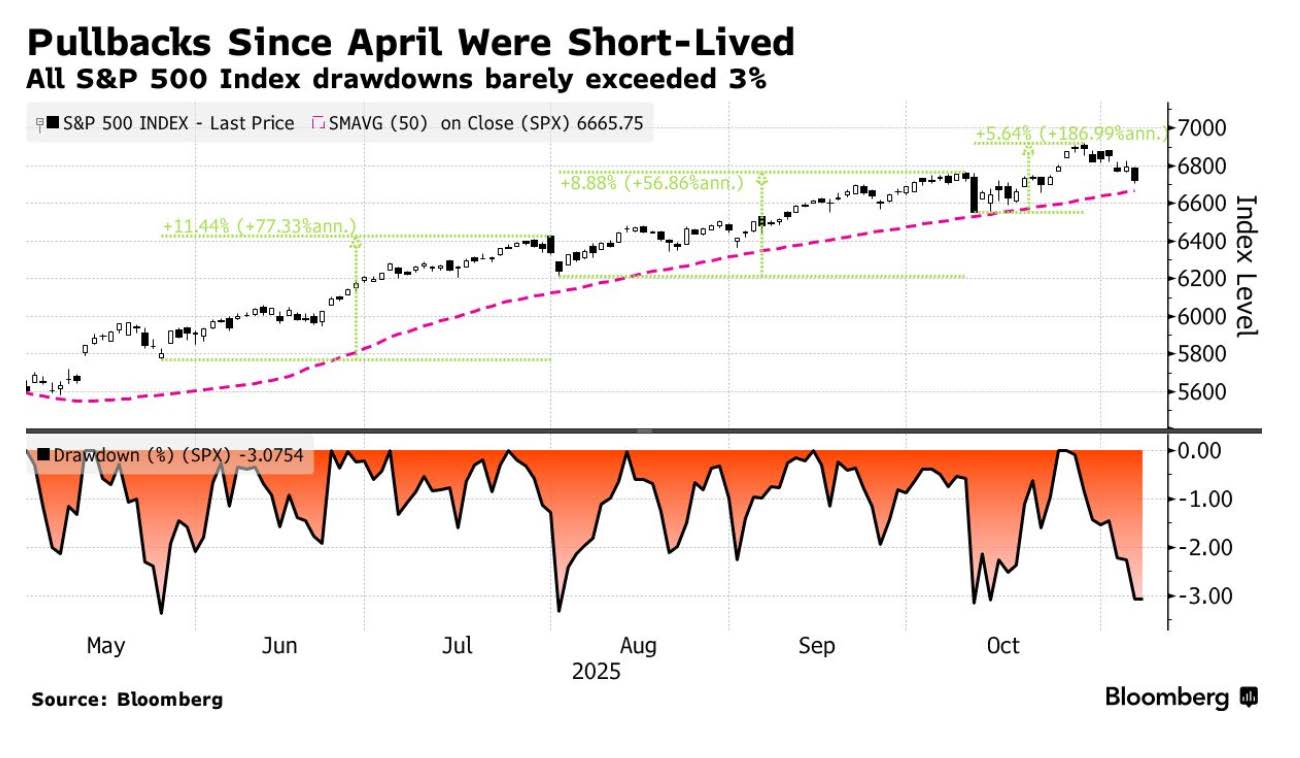

The chart below illustrates the current US market environment. Pullbacks don’t last. The one in November fit that pattern.

Granted, patterns end up changing. Anticipating when requires both research, intelligence, and luck.

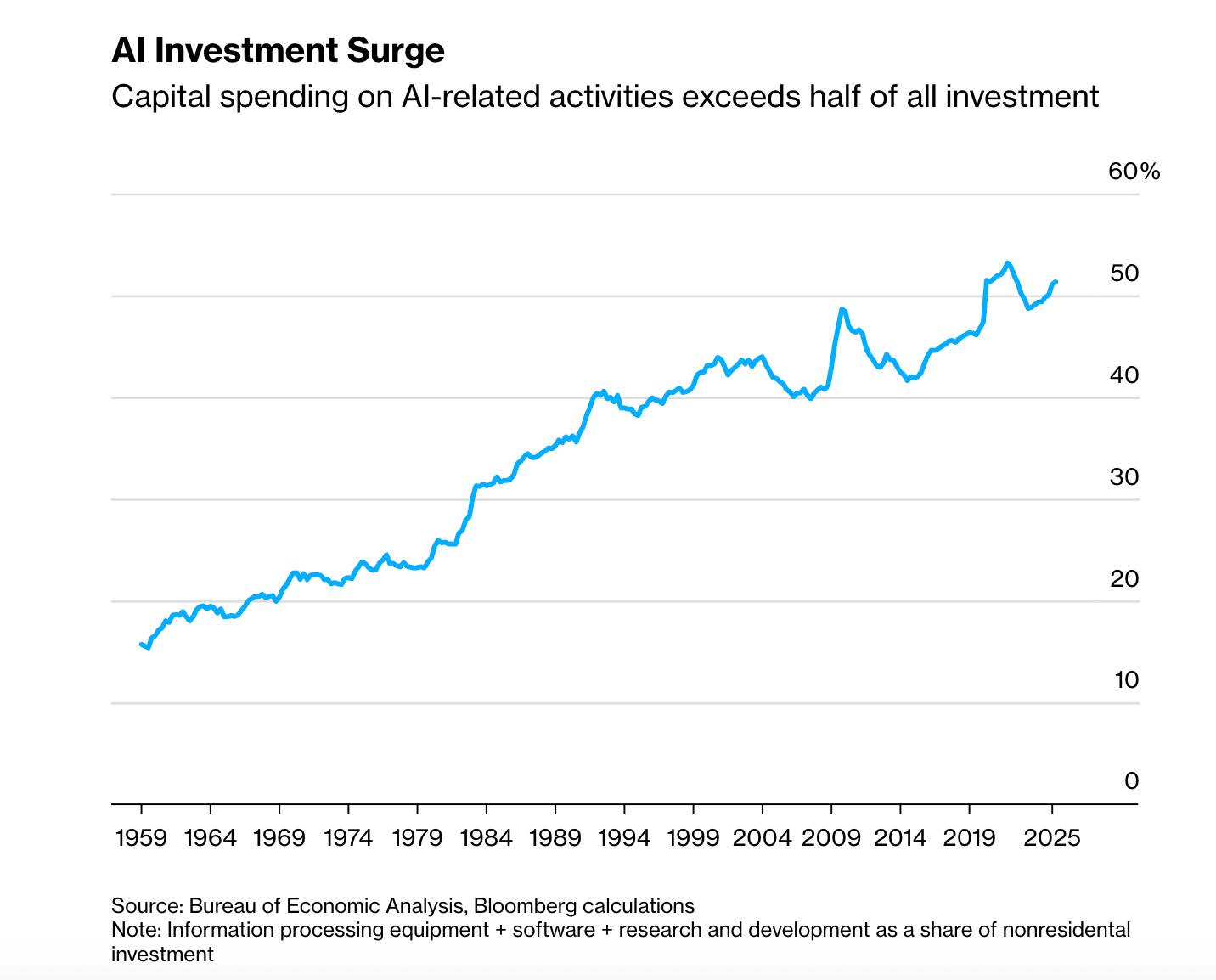

It is more than likely that the massive Artificial Intelligence (AI) infrastructure build-up has a lot to do with the difficulty that investors have to say when “too much is too much”. As shown in the chart below:

So far in 2025, AI-related investments account for about 50% of the total capital expenditures of the 500 corporations that comprise the S&P 500. This is just astounding. Given the totality of the data available, equity investors have concluded that continuing to invest in AI/tech makes sense despite the astronomical valuations.

In that context, during the past month, I continued to slowly reinvest part of the proceeds from maturing US Treasury investments into US equity ETFs (SPY, QQQ mostly), to benefit more significantly from the continuing uptrend. Also, part of the sale proceeds went into AGG to lengthen the duration of our fixed-income portfolios.

Conclusion

December is usually a positive month for US equities.

With a bit of luck, the FED will decide to facilitate a continuation of this pattern with a market-supporting interest rate cut next week. Failure to do so would probably result in a bout of market volatility. That said, as long as corporate earnings keep on trending upwards, a serious market drop is unlikely.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980