Overview

In October, the positive trend enjoyed by equities over the past seven months continued. The S&P 500 progressed another 2.34%. The Nasdaq, laden with growth tech stocks, jumped up 4.72%. The Russell 2000 (small cap index) was up 1.81%.

A variety of factors contributed to this positive performance, including better than expected corporate earnings, the Federal Reserve delivering on a .25% interest rate reduction and relatively subdued inflation data.

Internationally, the EPAC BM Index of developed economies (ex-US) rose a more moderate 1.61%, hampered by a rising USD, up 2% this month. Emerging markets did better, rising 4.12% for the MSCI Emerging market index.

One of the key factors behind this positive performance was the better than expected third quarter corporate earnings season that started over the second part of October, as shown below:

In October, US fixed income markets progressed. The US bond aggregate was up .62%. Investment grade and high yield corporate bonds gained .38% and .16% respectively.

Our median portfolio was up .56%. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 1.46%. Year to Date (YTD) our median portfolio is up 8.35% vs. 14.06% for our benchmark.

Market developments

The shutdown of the US government makes it harder for market watchers to evaluate the overall economic environment. A dearth of data makes the FED’s job harder. Nevertheless, the reduced number of data points in October included inflation numbers.

They showed that it is rising, but at a moderate pace.

Specifically, the Core US CPI stood at an annual rate of 3.01%, as of the end of September. It was at 2.92% at the end of August. There is no doubt about the direction of travel here. However, investors seem to think that this uptrend is manageable and probably temporary. The FED seems to concur, at least for now.

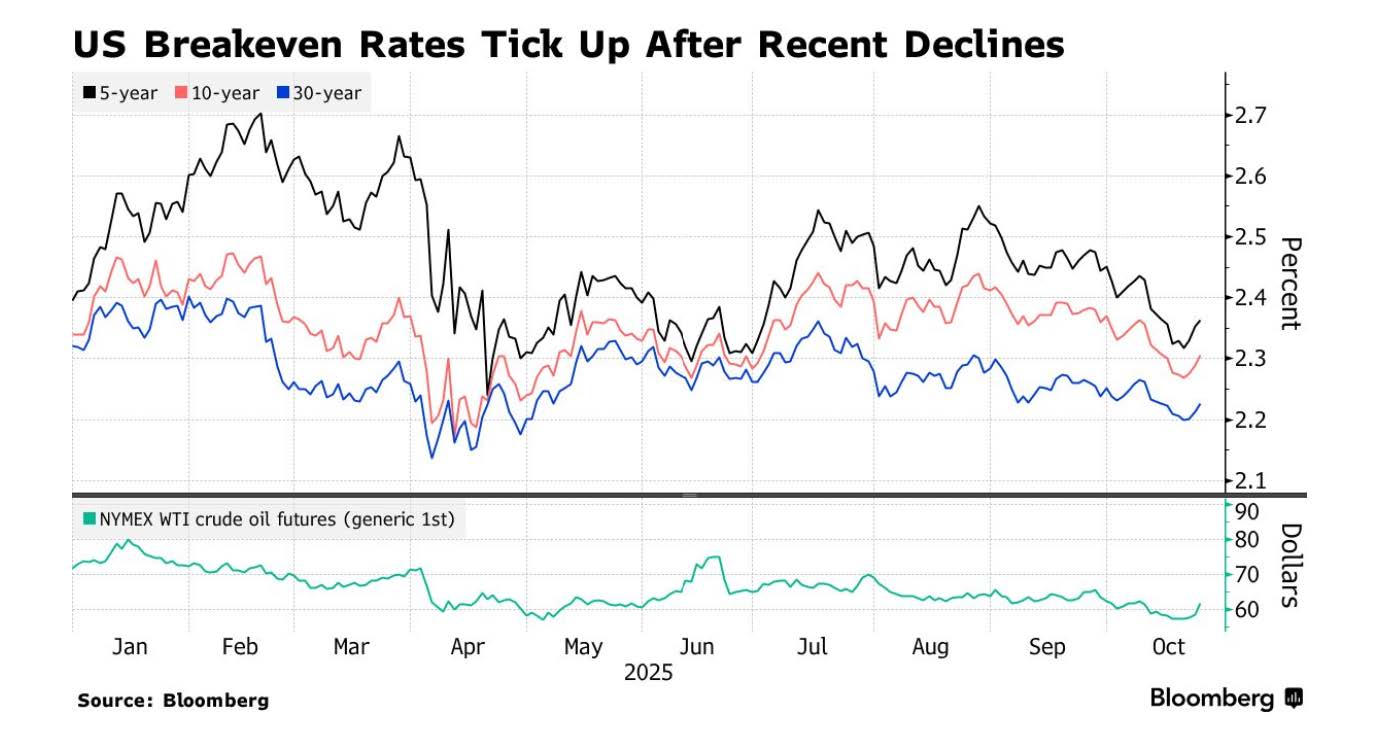

Here is a graph of inflation expectations, interpolated from interest rate yields:

The uptick is clear.

Looking ahead, the Artificial Intelligence (AI) investment binge, in the hundredth of billions, does not appear to be abating. It irrigates many industrial and service sectors of the economy.

While in more usual times, large capital expenditures in one sector of the economy would not suffice to support it in its entirety, it seems that the transformative nature of the AI revolution could upend this notion.

Portfolio Commentary

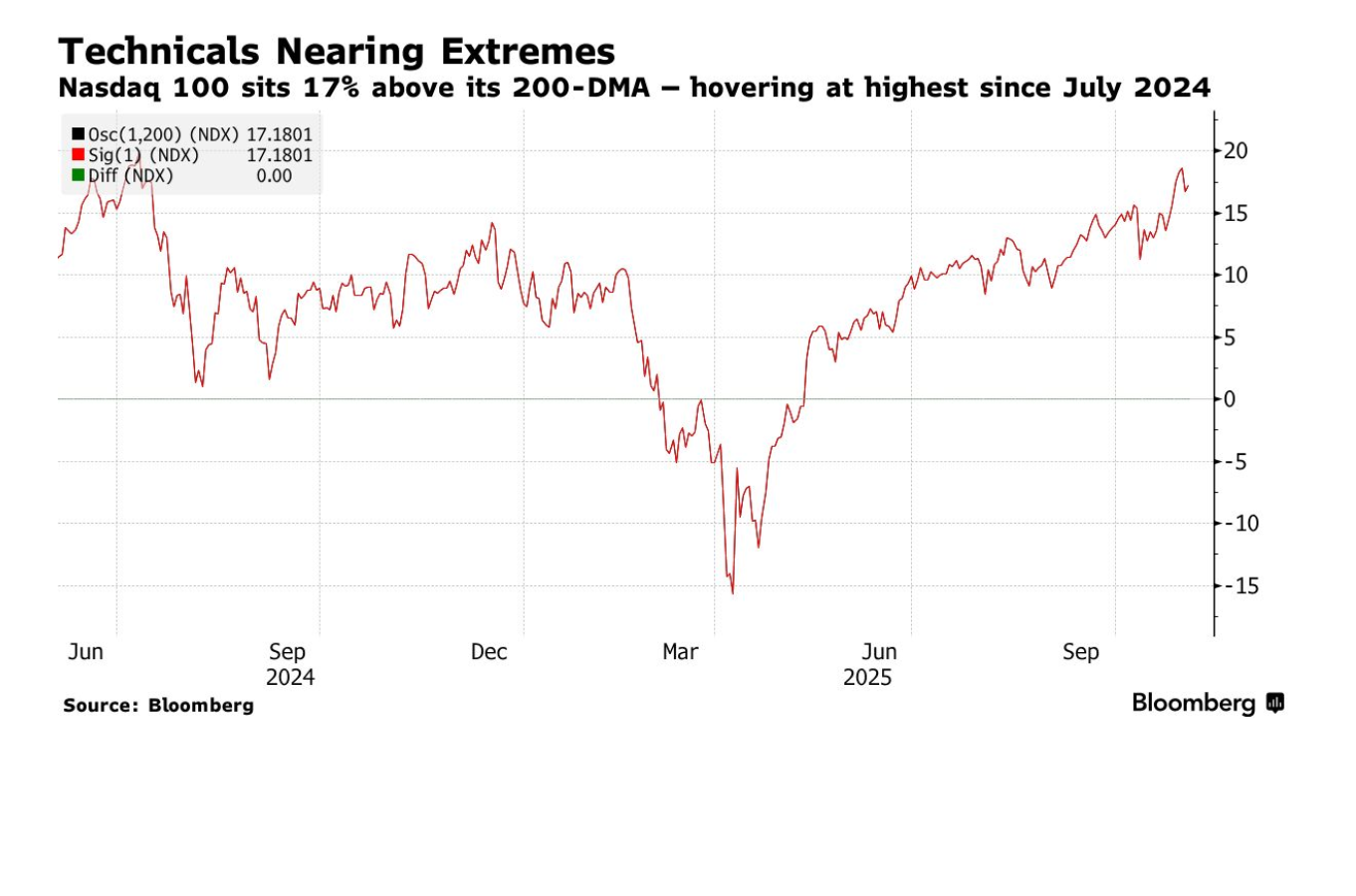

As you know, I have been reluctant to believe that the tariffs policy of the current US Administration would be of no consequences to the US economy and the world as a whole. US equity markets, and particularly the Nasdaq 100, seem to indicate otherwise and have jumped 30% up since their early April lows, as shown below:

This chart shows two main things: 1) The rebound from the April lows was historic in its speed and magnitude. In fact, it is one of only seven such rebounds since 1950., 2) tech valuations are historically stretched, and warning signs of an overheating condition abound.

In this context, I have proceeded cautiously with your portfolios. In the face of the unrelenting progression of the tech sector, I have partially switched out of RSP (equal weight S&P’s 500 ETF) in favor of SPY or QQQ. This will give us marginally more exposure to the Tech sector without increasing our overall equity exposure.

Additionally, I took some profit from our winning IAU (Gold ETF) positions. I sold IAU from qualified accounts only, to avoid adding to the significant capital gains generated this year on some accounts.

Despite valuations worries, I hesitate to sell more of our winning positions due to their potential fiscal impact. Only a major market drop, or the anticipation of one, would force me to do so. I do not see one yet, beyond a possible 5% to 10% downdraft.

Conclusion

Muddy waters. That’s what I think we are in.

Tech earnings are terrific. But the markets’ progression, outside of this sector, is often nil to uninspiring. Market indices are moving up on the back of ten mega capitalization stocks.

The narrowness of this advance is a cause for worry.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980