Overview

In October, the S&P 500 remained on its positive trendline, pushing up monthly performance another 3.65% overall, while the Nasdaq composite progressed 5.68% and the Russell 2000 (Small Cap stocks) gained 3.11%.

The FED delivered a .25% interest rate cut on September 17, as expected. Investors, who these days seem only to pay attention to the good economic news and to downplay the rest, decided to push US equity indices up as a result.

Internationally, the EPAC BM Index of developed economies (ex-US) rose a more moderate 2.16%. These developments arose in the context of a mixed economic picture.

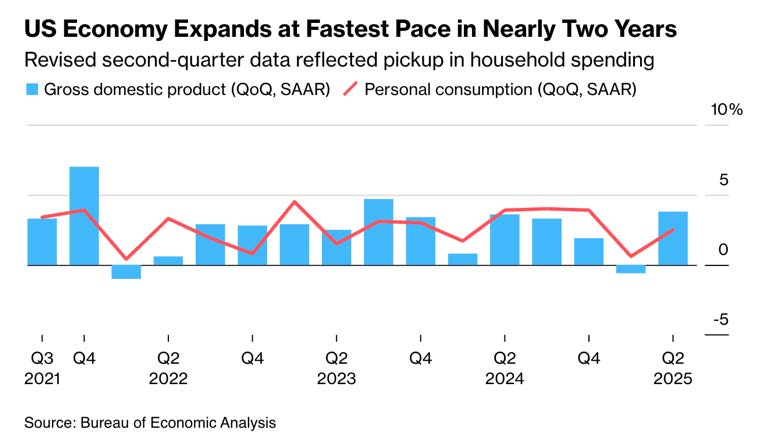

On the one hand, some data support the view that the US economy is fine, as shown in the GDP chart below:

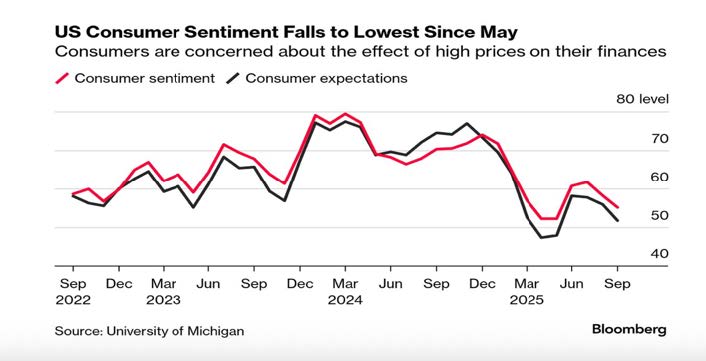

On the other hand, there is evidence that points in the opposite direction, as shown below:

In September, US fixed-income markets progressed. The US bond aggregate was up 1.09%. Investment-grade and high-yield corporate bonds gained 1.50% and .82%, respectively. Our median portfolio was up 1.92%.

Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 2.37%. Year to Date (YTD) our median portfolio is up 7.77% vs. 12.34% for our benchmark.

Market developments

The relentless rise of the US equity markets, over the past four months, has occurred in the context of mixed economic data that can legitimately sow doubts as to its sustainability.

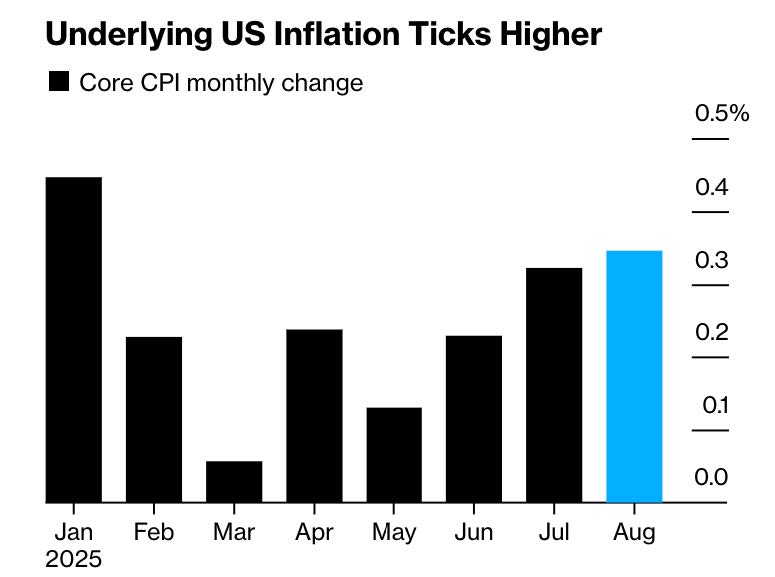

Inflation continues to rise, as shown below:

Additionally, labor market conditions are soft or deteriorating. Yet equities keep on rising.

For now, it seems that investors have accepted the storyline of an enduring artificial intelligence investment cycle and discounted high equity valuations and various signs of an economic slowdown.

Portfolio Commentary

Whatever my inclinations and beliefs about the economy and the current environment, I need to manage your assets based on both what signals the markets are sending and on what I think is likely to happen going forward.

Those signals and views are contradictory: 1) On the one hand, the markets have been relentlessly moving up since May in the context of a decidedly mixed economic panorama and, 2) On the other hand, my reading of the situation, both economically and otherwise, leads me to believe that this cannot last much longer.

At some point though, an investment manager needs to recognize that he may have to adjust his investment posture in the face of contradictions, be they real or perceived.

So, adjusting is what I have slowly started doing in September. Specifically, I invested some of the cash generated by maturing US Treasury investments back into equities. Overall, I have increased your equity

allocation by 5%. I do not intend to increase this pace until third quarter corporate earnings are released and surprise to the upside.

My deliberately slow tempo, when it comes to reinvesting in equity markets, is due to my sense that markets are stretched from a valuation standpoint, as confirmed in the chart below:

Conclusion

“Confusion de Confusiones” is the title of the first book ever written on stock trading and on the psychology of investors. It dealt with the operations of the Amsterdam stock exchange, sometimes around 1688, and about economic mania. It comes to my mind often these days.

The strength and resiliency of our equity markets surprise me. In the face of mixed economic news and destabilizing national and geopolitical developments, this resiliency, I will admit, confuses me; just as the

writer of “Confusion de Confusiones” was confused about what was happening on the Amsterdam stock exchange, almost four centuries ago and some forty years after the tulip bulbs mania.

This leads me to be very prudent and, as a result, to trail our benchmark as markets continue to rise. I hope that you understand my ambivalence and remain patient with my relative underperformance, so far this year.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980